The landscape of technological innovation is at a pivotal juncture, with the emergence of artificial intelligence poised to redefine how businesses operate and deliver value. At the heart of this transformation lies a critical distinction: the shift from selling tools to selling outcomes. As AI capabilities rapidly advance, particularly in large language models and generative AI, companies that offer software solutions are increasingly finding themselves positioned to disrupt traditional service-based industries. This evolution suggests that the next generation of trillion-dollar enterprises will likely be those that masterfully leverage AI to deliver comprehensive services, effectively blurring the lines between software and service provision.

The Intelligence vs. Judgment Divide in AI Adoption

A fundamental question preoccupies founders building AI tools: what happens when the next iteration of advanced AI models, such as those developed by OpenAI, Anthropic, or Google DeepMind, can perform the core functions of their products as mere features? This concern is valid, especially for businesses whose revenue models are centered on selling specific tools. Such companies operate in a race against the inherent improvement rate of the underlying AI models. Conversely, businesses that focus on delivering an outcome, rather than just the tool to achieve it, find that AI advancements make their services faster, cheaper, and more competitive.

Consider the example of financial management. A company might spend approximately $10,000 annually on accounting software like QuickBooks, while simultaneously incurring a significant $120,000 expense for an accountant to manage the closing of its books. The paradigm shift envisioned suggests that a future legendary company will simply offer a service that directly handles the entire book-closing process, encapsulating both the software and the human expertise, for a fraction of the combined cost. This illustrates the core principle: AI’s growing capacity to automate complex tasks is fundamentally altering the economics of service delivery.

The distinction between "intelligence" and "judgment" is central to understanding AI’s current impact and future trajectory. Writing code, for instance, is largely an exercise in intelligence. It involves applying known rules and complex algorithms to translate specifications into functional software. The process, while intricate, adheres to established protocols. Judgment, however, is a different faculty. It requires experience, intuition, and a nuanced understanding built over years of practice. This includes making strategic decisions about product development, prioritizing features, managing technical debt, and determining optimal release timing – areas where human insight has traditionally been indispensable.

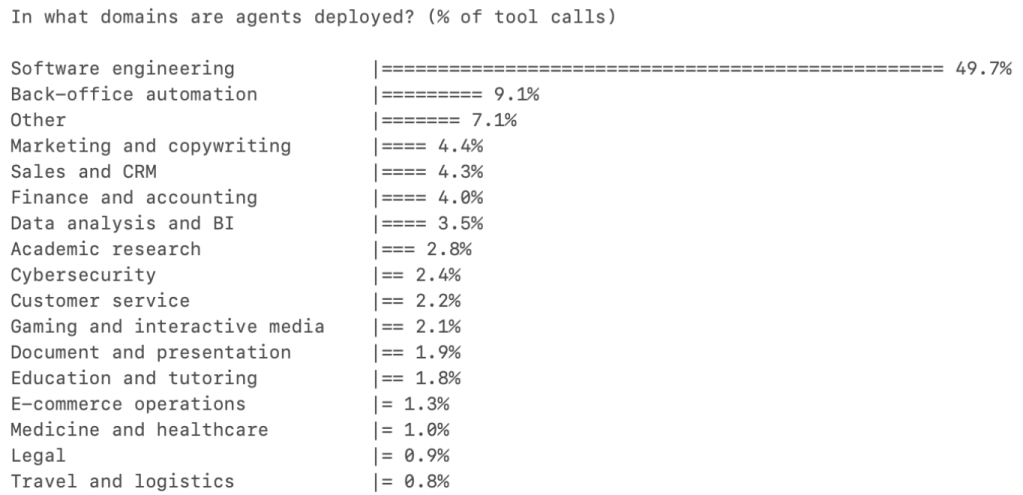

A year ago, the predominant use of AI in professional settings, such as with tools like Cursor, was primarily as an advanced autocomplete feature. Professionals used AI to augment their existing workflows, leveraging it for tasks that required intelligent execution. Today, a significant shift is evident. In many domains, AI agents are initiating tasks rather than merely assisting humans. The field of software engineering has emerged as a leading adopter, accounting for over half of all AI tool usage across various professions. This dominance is attributed to the inherently "intelligent" nature of software development, which AI models are increasingly capable of handling autonomously. The remaining 50% of AI tool usage is distributed across other professions, with each sector still in its nascent stages of AI integration. The reason for software engineering’s head start lies in its composition: it is predominantly intelligence work, a domain where AI has now crossed a critical threshold, enabling it to perform most of these tasks autonomously and leave the judgment-centric aspects to human professionals. This transition is not confined to software development; it is anticipated to permeate every profession.

From Copilots to Autopilots: Redefining Service Delivery

The evolution of AI tools can be broadly categorized into two models: copilots and autopilots. A copilot is an AI assistant that augments human capabilities, empowering professionals to perform their jobs more efficiently. An autopilot, conversely, is designed to deliver an entire service or outcome autonomously.

Historically, as AI models were still developing their intelligence and judgment capabilities, the most effective approach was to develop copilots. These tools placed AI directly into the hands of experienced professionals, allowing them to harness its power as they saw fit. Companies like Harvey, which provides AI solutions for law firms, and Rogo, serving investment banks, exemplify this model. In these scenarios, the professional is the primary customer, the AI tool enhances their productivity, and they retain responsibility for the final output. This approach leverages existing expertise and allows businesses to gradually integrate AI without fundamentally altering their service delivery model.

However, the rapid advancement of AI models has enabled a transition to the autopilot model in certain categories. Today, in some fields, the most effective entry point is to offer a fully automated service. For instance, a company like Crosby might offer to draft an NDA directly for a business that needs one, rather than selling an AI tool to a law firm to do it. Similarly, WithCoverage aims to provide insurance directly to CFOs, bypassing traditional brokers. In this model, the customer is purchasing the outcome directly. The budget allocated to services within any profession typically dwarfs the budget for tools. Autopilots, by capturing this "work budget" from day one, are positioned for significant growth. The higher the proportion of "intelligence work" within a given field, the sooner the adoption of autopilot solutions is likely to occur.

The Convergence of Copilots and Autopilots

The trajectory of AI development suggests a future where today’s "judgment" will become tomorrow’s "intelligence." As AI systems accumulate vast proprietary datasets that capture the essence of good judgment within specific domains, the boundaries between human and artificial decision-making will continue to blur. This continuous learning loop means that copilots and autopilots are not mutually exclusive concepts but rather stages in a continuum. The transition from a copilot-centric approach to an autopilot-centric one has already begun in numerous sectors. However, the initial strategy adopted by an AI company significantly influences its ability to capture customers and leverage data for future advancements. Companies that start as autopilots are better positioned to win customers immediately and build the data moats necessary to eventually handle even the most complex judgment-driven tasks.

The Autopilot Playbook: Outsourcing as the Strategic Entry Point

The economic reality of modern business reveals a significant imbalance: for every dollar spent on software, approximately six dollars are spent on services. This substantial services market represents the total addressable market (TAM) for autopilots, encompassing both insourced and outsourced labor. However, the most strategic entry point for AI-driven services lies where outsourcing already exists.

When a task is already outsourced, it signifies several key business realities:

- Acceptance of External Execution: The company has already acknowledged that the work can be effectively performed by external entities.

- Pre-existing Budget Allocation: There is an established budget line item that can be cleanly substituted with an AI-powered service.

- Outcome-Oriented Purchasing: The buyer is already accustomed to purchasing a defined outcome rather than a specific process or tool.

Replacing an existing outsourcing contract with an AI-native service provider is a straightforward vendor swap. In contrast, replacing internal headcount with AI automation constitutes a more complex organizational restructuring.

The effective playbook for AI-driven service companies, therefore, is to initially target outsourced, intelligence-heavy tasks. Success in this phase hinges on mastering distribution channels and customer acquisition. Subsequently, as the AI compounds its capabilities and data, the company can strategically expand into insourced, judgment-heavy work. The outsourced task serves as a critical wedge, opening the door to the larger TAM represented by insourced labor.

A prime example is the legal sector. Companies like Crosby have focused on tasks such as drafting Non-Disclosure Agreements (NDAs). NDAs are well-defined, primarily intelligence-driven tasks that many companies already outsource to external legal counsel. The existing budget for this service, coupled with a clear scope and immediate return on investment (ROI), makes it an attractive proposition for AI automation. The substitution of an outsourcing contract with an AI-native service for NDA drafting is a frictionless transition for the client.

Mapping the Opportunity: A Spectrum of AI Service Potential

To identify the most promising avenues for AI-driven services, a strategic mapping exercise is essential. This involves plotting various service verticals along two key dimensions: the spectrum from intelligence-intensive to judgment-intensive work, and the ratio of outsourced to insourced labor. The resulting "opportunity map" provides a priority framework, with the potential labor TAM indicated in brackets for each sector.

Key Service Verticals for AI Autopilot Disruption:

-

Insurance Brokerage ($140-200 Billion TAM): The commercial lines of insurance are highly standardized. The core value proposition of a traditional broker—shopping across carriers and completing forms—is essentially an intelligence-driven task. The distribution layer is fragmented, with thousands of small brokers operating independently, meaning no single incumbent holds a dominant customer relationship. This fragmentation creates an ideal environment for AI-native providers like WithCoverage and Harper to offer streamlined, outcome-based insurance solutions.

-

Accounting and Audit (>$50-80 Billion Outsourced in the U.S.): The United States faces a significant structural shortage of accountants. Over the past five years, the profession has lost approximately 340,000 professionals, while demand continues to rise. Compounding this issue, 75% of Certified Public Accountants (CPAs) are nearing retirement, the path to licensing is arduous, and starting salaries often lag behind those in technology and finance. This persistent shortage is accelerating the adoption of AI solutions in accounting firms, more so than in many other professions. Companies like Rillet are developing AI-native Enterprise Resource Planning (ERP) systems designed to automate the entire book-closing process, while Basis began as a copilot for accountants, demonstrating a phased approach to AI integration.

-

Healthcare Revenue Cycle Management (>$50-80 Billion Outsourced in the U.S.): While "healthcare" often implies complex judgment, the billing and revenue cycle management layer is predominantly an intelligence-intensive domain. Medical coding, for instance, involves translating clinical notes into one of approximately 70,000 standardized ICD-10 codes. Although the rules are intricate, they are codified and predictable. The outsourcing market for these services is already mature and outcome-based, making it ripe for autopilot disruption. An AI autopilot simply needs to perform these tasks more efficiently and at a lower cost. Anterior is recognized as a leader in this space.

-

Claims Adjusting (>$50-80 Billion including Third-Party Administrators – TPAs): On the other side of the insurance policy, claims adjusting represents another significant opportunity for autopilot solutions. For standard insurance lines, claims settlement involves interpreting policy language against damage assessments and setting reserves based on actuarial data. The workforce of claims adjusters is aging, with limited new entrants to replace them. The market is heavily outsourced to independent adjusters and TPAs such as Crawford and Sedgwick. This presents two distinct autopilot opportunities within a single industry: one for claims handling itself, with companies like Pace building AI solutions, and another for AI-native TPAs, such as Strala.

-

Tax Advisory ($30-35 Billion TAM): Although CPA licensing creates a regulatory barrier to entry, 80-90% of the underlying tax advisory work is intelligence-based. As AI tax solutions expand their coverage to additional jurisdictions, their data moats deepen. The complexity of multi-jurisdiction tax laws is a burden for Small and Medium-sized Businesses (SMBs), who often outsource this function due to the difficulty of maintaining in-house expertise. Companies like TaxGPT are early movers, alongside European players like Skalar and Ravical, demonstrating the global potential of AI in tax.

-

Legal Transactional Work ($20-25 Billion TAM): Tasks such as contract drafting, NDA generation, and regulatory filings fall into the category of high-intelligence, routinely outsourced legal work. The standardized nature of these work products allows for verifiable quality, enabling clients to trust AI-generated output without requiring extensive legal review. Harvey has emerged as a leader in this space and is rapidly transitioning towards autopilot solutions, while newcomers like Crosby and Lawhive are building natively as autopilots.

-

IT Managed Services (>$100 Billion TAM): Virtually all SMBs outsource their IT functions. Routine tasks such as patching, monitoring, user provisioning, and alert triage represent intelligence work performed repeatedly across numerous identical IT environments. Existing software providers like ConnectWise and Datto offer tools to Managed Service Providers (MSPs). However, there is a significant opportunity for a company to offer "your IT runs" directly to businesses as a managed outcome. Edra is focused on automating IT processes, while Serval is automating IT support functions.

-

Supply Chain and Procurement (>$200 Billion TAM): Large enterprises typically engage in deep negotiations with their top 20% of suppliers. The remaining long tail of suppliers often receives minimal attention due to the economic inefficiency of manual engagement. Contract leakage, where negotiated terms are not fully realized, can account for 2-5% of total procurement spend. The "wedge" opportunity here lies in automating these neglected areas. By addressing "abandoned work," companies can unlock value without needing to justify new budget lines or displace established incumbents. Magentic is developing AI for direct procurement, AskLio for indirect procurement, and Tacto is building both the system of record and a copilot for the mid-market.

-

Recruitment and Staffing (>$200 Billion TAM): This represents one of the largest services markets. The initial stages of the hiring funnel—screening resumes, matching candidates, and outreach—are primarily intelligence-driven. However, securing a candidate and assessing cultural fit require judgment, honed by years of pattern recognition. The autopilot opportunity exists in high-volume, low-judgment roles where candidate matching is standardized. Companies such as Juicebox, Mercor, and Jack & Jill are emerging leaders developing solutions across this spectrum.

-

Management Consulting ($300-400 Billion TAM): While a vast market, management consulting work is predominantly judgment-based. The key question is whether AI can effectively disaggregate consulting into its constituent parts: intelligence components (data gathering, benchmarking) and judgment components (strategic recommendations). If the intelligence layer can be automated, the judgment layer may remain human-centric. The leading candidates for AI disruption in this sector are still emerging.

The Future Landscape: Pure-Play Autopilots and the Innovator’s Dilemma

In 2025, the fastest-growing AI companies were predominantly copilots, offering tools to enhance existing professional workflows. As we move into 2026 and beyond, many of these companies will undoubtedly attempt to transition into autopilot providers. They possess established products and deep customer knowledge, providing them with a significant advantage.

However, these incumbents face the "innovator’s dilemma." By selling comprehensive services (the work itself), they risk disintermediating their own customer base, which consists of professionals who currently perform that work. This creates a critical opening for "pure-play" autopilot companies. These new entrants, unburdened by existing customer relationships with service providers, can focus exclusively on building and scaling AI-native services from the ground up, directly targeting the end-customer outcome.

For founders and investors building in this space, the strategic imperative is clear: identify service verticals where intelligence work is abundant, outsourcing is prevalent, and the potential for outcome-based AI automation is high. The next trillion-dollar companies will not simply offer smarter tools; they will offer smarter, more efficient, and more cost-effective ways to get work done.

For further insights or to discuss opportunities in this rapidly evolving sector, contact Julien at [email protected] or follow him on X @julienbek.

{kind=link}