Tokenized Real World Assets (RWAs) have rapidly emerged as a pivotal narrative within the decentralized finance (DeFi) ecosystem, promising to bridge traditional financial instruments with blockchain’s efficiency and transparency. While the sector has already surpassed $20 billion in tokenized assets, predominantly U.S. Treasuries, private credit, a significantly larger and more diverse asset class in traditional finance, remains largely untapped due to a persistent and critical challenge: liquidity. Issuers of tokenized private credit, such as those facilitated by platforms like Centrifuge, mint share tokens representing claims on real funds generating real yield. However, these tokens often become illiquid, effectively locking holders until maturity or slow, gated redemption windows. The Net Asset Value (NAV) displayed on dashboards serves merely as a reference price, not a dynamic market price, undermining the very premise of on-chain tradability. Agra Bonds, operating at bonds.agra.gg, has emerged as a crucial beta-stage initiative on Ethereum, directly addressing this liquidity gap by establishing a specialized orderbook for tokenized credit.

The Liquidity Conundrum in Tokenized Private Credit

The vision for tokenizing private credit is compelling: unlock capital efficiency, broaden investor access, and enhance transparency for an asset class traditionally characterized by opacity and high barriers to entry. Private credit, which encompasses non-bank lending to private companies, has witnessed exponential growth in traditional finance, reaching trillions of dollars globally. Its appeal lies in higher yields compared to public markets, driven by illiquidity premiums and specialized underwriting. When brought on-chain, however, the inherent illiquidity of private credit presents a unique hurdle.

Unlike highly liquid and standardized assets like U.S. Treasuries, which can leverage existing decentralized exchange (DEX) infrastructure due to their homogeneity and stable NAVs, private credit instruments are inherently heterogeneous. Each fund or loan has distinct coupons, durations, credit curves, and underlying collateral, making a constant NAV an impossibility. This complexity renders Automated Market Makers (AMMs), the dominant liquidity primitive in DeFi, largely unsuitable for tokenized private credit. AMMs, designed for assets that trade within relatively stable pairs or along predictable bonding curves, struggle to accurately price the narrow yet information-rich band around NAV that characterizes these instruments. Consequently, holders of tokenized private credit often find themselves in a bind, unable to exit positions efficiently, which stifles institutional adoption and limits the scale of primary issuance. This structural bottleneck has plagued the RWA thesis for over two years, prompting a search for more tailored solutions.

Agra Bonds Emerges: A Specialized Solution for On-Chain Credit Trading

Agra Bonds steps into this void with a focused and pragmatic approach: a central limit orderbook (CLOB) tailored specifically for tokenized credit on the Ethereum blockchain. Its distinguishing feature is quoting in yield and discount-to-NAV terms, rather than raw price. This methodology directly mirrors how traditional finance (TradFi) credit desks originate and trade such instruments, providing a familiar and intuitive interface for sophisticated investors.

The platform enables market makers to post bids and asks denominated in basis points of discount or premium relative to the token’s reference NAV. The user interface then dynamically translates these quotes into an effective yield, factoring in the instrument’s coupon and duration. Takers can then interact with the orderbook in a manner consistent with any CLOB, with settlement occurring peer-to-peer directly between buyer and seller wallets via a smart contract. This design eliminates the need for vaults, AMM pools, or shared liquidity reserves, reducing counterparty risk and enhancing capital efficiency.

The decision to opt for a CLOB over an AMM is strategic. Tokenized bonds and credit shares typically trade within a tight band around their NAV, often just a few percentage points in either direction. This band is laden with crucial information regarding credit quality, duration, and liquidity preferences. An AMM would struggle to price these nuances effectively, potentially leading to inefficient markets and significant slippage. A CLOB, by contrast, allows for precise price discovery based on supply and demand dynamics, reflecting the true market sentiment for these complex financial instruments. Agra is not attempting to be a general DEX for all RWAs; it is carving out a niche as a specialized credit desk for bond-like tokenized assets.

Inside Agra Bonds: Mechanics and User Experience

From a user perspective, Agra Bonds offers a straightforward experience typical of on-chain trading venues. Users connect their Ethereum-compatible wallets, and any necessary Know Your Customer (KYC) requirements associated with the underlying instrument are enforced at the contract level. For instance, the ACRDX share token, a flagship asset on Agra, incorporates transfer restrictions, ensuring that only whitelisted wallets can receive it, even if a trade clears the orderbook. This robust, on-chain KYC enforcement is critical for maintaining compliance with regulatory frameworks governing private credit.

Once connected and cleared, users can post limit orders or sweep the top of the orderbook, executing trades directly. Post-settlement, positions are held as standard ERC-20 balances in the user’s wallet. This adherence to the ERC-20 standard is vital for composability within the broader DeFi ecosystem. It means that tokens acquired on Agra Bonds can potentially be used as collateral on any lending market that chooses to list them, significantly enhancing their utility and unlocking new financial primitives. This composability pitch is a key driver for issuers, as a liquid secondary market elevates the potential applications and perceived value of their tokenized paper for downstream integrators.

Live Markets and Their Significance (As of Late April 2026)

Agra Bonds currently features three operational markets, each offering insights into its capabilities and strategic intent:

-

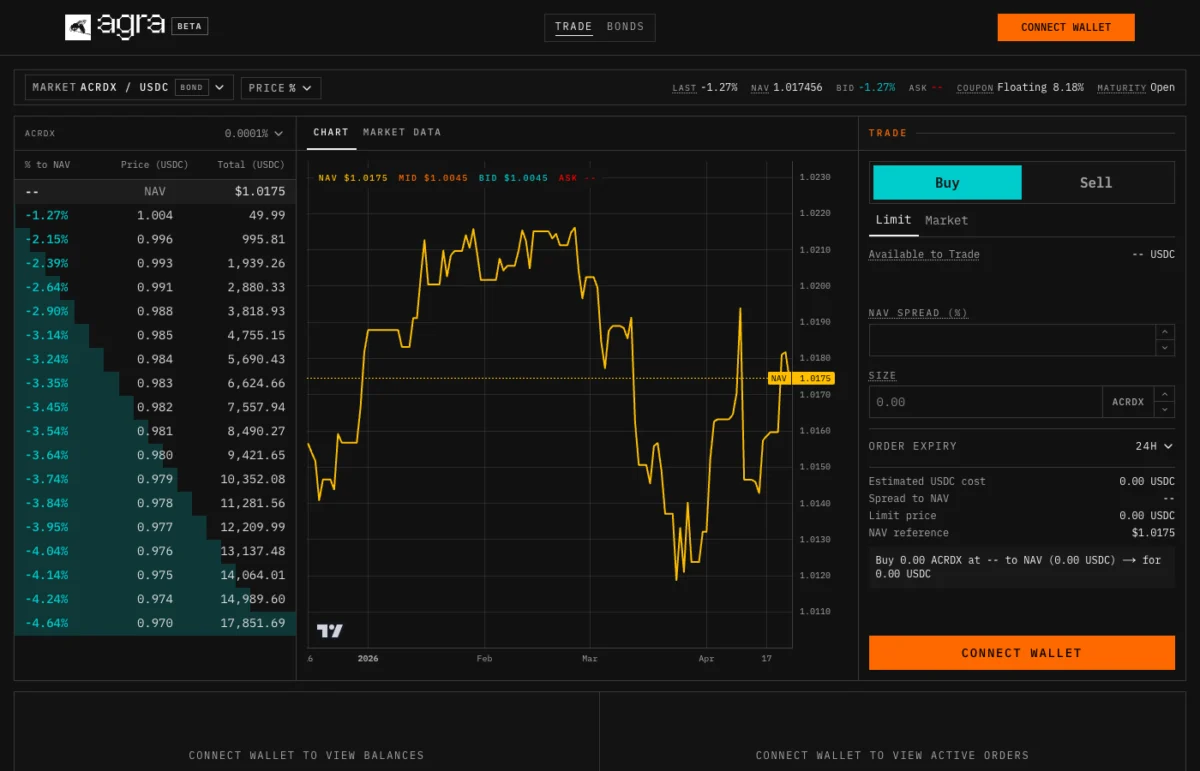

ACRDX/USDC: This is Agra’s flagship market. The underlying asset is Anemoy’s tokenized wrapper of the Apollo Diversified Credit Fund, a senior private-credit fund managed through a British Virgin Islands (BVI) vehicle. Access to this fund requires KYC for transfers. The NAV typically hovers around $1.016, with a floating coupon rate of approximately 8.18%. The fund has an open-ended maturity. Orderbooks for ACRDX/USDC commonly show bids ranging from a 1% to 7% discount-to-NAV, with greater capacity available at deeper discounts. A buyer engaging with the best bid secures the 8.18% coupon yield, plus any pull-to-NAV accrual if the position is eventually redeemed at par. This compensates for the inherent illiquidity and the senior-private-credit default risk associated with a BVI-domiciled vehicle.

-

pALPHA/USDC: This market features Pharos Network’s tokenized consumer credit, which is structured as a multi-tranche instrument with partial guarantees. It is onboarded through the same Centrifuge/Anemoy stack. As expected given its credit profile, liquidity for pALPHA is generally thinner than for ACRDX, and the discount band tends to be wider, reflecting higher perceived risk and lower liquidity.

-

aEthWETH/WETH: This market, launched opportunistically by Agra, demonstrates the platform’s agility in response to market dislocations. It was initiated in the aftermath of the KelpDAO rsETH exploit, an event that significantly impacted Aave’s rsETH markets and caused a sharp increase in WETH utilization within Aave’s Ethereum pool. KelpDAO’s rsETH is a liquid staking token (LST), and its exploit created systemic stress. aEthWETH represents the Aave supply receipt for WETH. By creating a secondary market for aEthWETH, Agra provided depositors with a crucial exit ramp for their supply positions without having to wait for Aave’s utilization to normalize or for complex bad-debt accounting to be resolved. While the capacities in this market are modest and its use case tactical rather than structural, it effectively showcased how quickly a rate-quoted CLOB can be deployed to provide liquidity for a distressed asset in a volatile environment.

Public data on cumulative trading volume for Agra Bonds is not yet published, and the platform lacks a public dashboard. However, live order books generally display capacity in the low-to-mid six figures of USDC per price level. While typical for a beta RWA venue, this depth remains significantly below what would be considered institutional-grade for a serious private-credit desk.

Trust Architecture: Asset vs. Exchange

Understanding the trust model of Agra Bonds requires distinguishing between two distinct layers: the underlying asset and the exchange venue itself.

The asset layer is largely transparent and inspectable. The ACRDX share token (address: 0x9477724Bb54AD5417de8Baff29e59DF3fB4DA74f) is a verified Solidity 0.8.28 ShareToken contract. It conforms to a standard Centrifuge-style RWA primitive: an ERC-20 token with EIP-2612 permits, a MakerDAO-style wards authorization pattern for minting, burning, and configuration, and critical transfer-restriction hooks that enforce KYC on-chain. A vault mapping links the share token to its underlying Centrifuge pool for NAV reference. The code is public, and this pattern has been widely adopted by multiple issuers, allowing for direct evaluation of its inherent risks. It is important to note that this token model is centralized by design. Authorized operators (e.g., Anemoy as the issuer) retain the ability to mint, burn, pause transfers via hooks, and reconfigure the vault pointer. For regulated private credit, this is not a vulnerability but a necessary feature. Issuers must have the capacity to enforce redemptions, blacklist sanctioned addresses, and gate funds if the underlying vehicle faces issues. Therefore, a buyer of ACRDX implicitly trusts Anemoy, the issuer, and this trust boundary is explicit and factored into the instrument’s pricing.

The exchange layer, however, presents a different level of transparency. Each Agra market operates behind an ERC-1967 proxy, referenced in the UI via a market query parameter. These proxies are responsible for handling order placement, matching, and settlement against the underlying share token and USDC. As of this writing, the source code for these orderbook contracts is not verified on Etherscan, no public audit reports have been posted, and there is no public GitHub repository detailing the matching logic. While settlement is on-chain and non-custodial—meaning funds move directly between maker and taker wallets—the underlying logic that routes these transactions through the proxy contracts is not currently readable by users. This opacity is not uncommon for a beta venue, but it represents a significant variable that must be addressed before the platform can achieve institutional scale. A subtle flaw in a CLOB’s logic might not manifest immediately in the UI but could emerge in an obscure edge case months later, potentially leading to unforeseen issues.

The Competitive Field for RWA Secondary Markets

The market segment targeted by Agra Bonds is niche, yet crucial, and increasingly competitive. The absence of robust secondary liquidity for tokenized credit has been the primary impediment to the broader adoption of the RWA thesis. Issuers acknowledge this, and many institutional buyers are reluctant to scale positions without clear exit strategies. Various venues are attempting to solve this problem, each with a different approach.

-

Figure Markets: This is arguably Agra’s closest direct competitor, operating an on-chain limit-order book for tokenized credit on its proprietary Provenance blockchain. Figure is significantly larger, more institutionally focused, and handles substantial volume in Home Equity Line of Credit (HELOCs) and private credit. However, it operates within a highly regulated, permissioned environment, making it largely inaccessible to most general DeFi users.

-

NewEra Finance: On the DeFi side, NewEra is another close analog, positioning itself as a multi-chain secondary market for a broader range of RWAs, including bonds and equities. However, NewEra employs an AMM-style aggregator rather than a pure orderbook, which, as discussed, may be less suitable for the intricacies of private credit.

-

Bondi Finance: This platform offers a tokenization-plus-secondary stack with a specific focus on corporate bonds and Sukuk (Islamic financial certificates).

-

IXS and Swarm Markets: These entities occupy adjacent niches, with IXS focusing on regulated decentralized exchanges and Swarm Markets on over-the-counter (OTC) trading.

It is important to differentiate Agra from origination-first credit protocols such as Maple Finance, Clearpool, Goldfinch, TrueFi, and Centrifuge itself. While these platforms are instrumental in issuing credit positions, their primary business model does not involve running meaningful secondary markets for those positions. They typically anticipate holders to redeem their assets at maturity rather than actively trade them.

Furthermore, solutions employed by platforms like Ondo Finance and BlackRock’s BUIDL fund for tokenized Treasuries are not directly applicable to private credit. These platforms route secondary flow through standard DEXes, a strategy that works effectively for Treasuries due to their homogeneity and constant NAV. This approach fails for private credit, where each instrument has unique characteristics and a fluctuating NAV.

Finally, protocols like Pendle and Notional Finance operate in the adjacent space of yield tokenization and fixed-rate trading. They allow users to separate and trade the yield component from the principal component of an asset rather than trading the underlying bond itself. While complementary to Agra’s mission by enhancing yield-curve primitives, they are not direct competitors in the secondary market for the principal asset.

Agra’s competitive advantage lies in its sharp focus. It is one of the few DeFi-native venues offering a yield-quoted CLOB specifically for Ethereum tokenized private credit. Its direct integration into the Centrifuge issuer pipeline provides a strong foundational ecosystem, and its ability to rapidly deploy opportunistic markets, such as the aEthWETH book, showcases its technical agility. However, its current lack of verified contract source, published audit trails, and broad issuer diversity are areas where competitors, particularly institutional players like Figure, hold a significant lead.

Addressing the Risks Worth Tracking

As a beta-stage platform operating in an nascent yet critical segment of DeFi, Agra Bonds carries several risks, none of which are unique to its specific implementation but are inherent to its operational stage and asset class.

-

Contract Opacity: This is the most pressing technical risk. The orderbook proxies, which manage crucial functions like order placement, matching, and settlement, remain unverified on Etherscan and unaudited publicly. While current settlement mechanisms appear functional and the UI-to-contract path seems clean, the absence of publicly inspectable matching logic or details regarding proxy upgrade controls introduces a layer of trust. For a production-grade credit venue aiming for institutional adoption, publishing its source code and undergoing comprehensive, independent audits are non-negotiable requirements. Until these steps are taken, users engaging with the platform must acknowledge that they are effectively relying on a "trust-the-frontend" model at the exchange layer, necessitating cautious position sizing.

-

Liquidity Depth: The current order books, while functional, are shallow by institutional standards. This implies that round-trip costs for transactions larger than the immediate top level of liquidity can be material. More critically, the platform’s ability to facilitate large-scale exits during stress scenarios—precisely the use case it aims to address—remains untested. The aEthWETH market, while a commendable demonstration of agility, was relatively small, and its behavior in a true market-wide stress event involving substantial volume is yet to be observed. Deeper liquidity is essential to attract larger capital allocators and to prove the platform’s resilience.

-

Underlying Credit Risk: This fundamental risk is often understated in the broader DeFi discourse surrounding RWAs. While ACRDX represents senior paper in a diversified fund, which implies a relatively sound credit profile, it remains private credit. Its BVI domicile introduces jurisdictional considerations, and the effective yield of approximately 9-10% at current discounts is compensation for real default risk, not a "risk-free" yield. Any buyer engaging with the orderbook, particularly at a discount, is taking a direct view on the underwriting quality of Apollo, the fund manager, rather than solely on the security model of Ethereum. It is entirely possible for the Agra platform to function flawlessly as advertised, yet a buyer could still incur losses if the underlying fund encounters credit difficulties. This distinction is paramount for DeFi users accustomed to different risk profiles.

Notably, Agra Bonds currently features no proprietary AGRA token, no points program, and no yield farming layer. This is a deliberate design choice and, in the context of a credit venue, should be considered a feature rather than an omission. Layering reflexive incentive structures on top of instruments whose returns are inherently bounded by their coupon can introduce unnecessary complexity and misaligned incentives, potentially destabilizing the market.

The Broader Implications for RWA Infrastructure

The RWA category’s journey to unlock its full potential hinges on resolving the secondary liquidity problem, particularly for private credit. A functional, rate-quoted CLOB for Ethereum-based credit would represent a foundational piece of infrastructure, enabling the next phase of growth. Once holders can confidently exit positions at a market-cleared discount, a positive feedback loop can commence:

- Issuers gain the confidence to sell larger primary tranches of tokenized private credit.

- Lending protocols become more willing to accept these tokens as collateral, setting tighter risk parameters based on real-time market prices rather than static NAVs.

- The entire duration stack of tokenized credit begins to resemble the mature, liquid markets seen in traditional finance.

Agra Bonds, despite being early, small, and having clear gaps to close—namely, verified contracts, public audits, a broader issuer set, and more issuer-funded inventory—is uniquely positioned. It is one of the few venues addressing the right problem with the right primitive. The competitive landscape for this specific niche is still fluid, with incumbents like Figure (institutional) and NewEra (DeFi, AMM-based) not yet having fully locked down the category. Agra’s existing relationships within the Centrifuge ecosystem provide a defensible starting point.

Over the coming two quarters, three key milestones will determine Agra’s trajectory:

-

Onboarding a second issuer category not routed through Centrifuge: This is arguably the most critical. As long as all assets on the platform originate from a single share-token pipeline (Centrifuge), Agra structurally remains a feature of Centrifuge rather than a standalone credit venue. A new issuer, such as Superstate, Backed, or Maple, would demonstrate Agra’s independence and its ability to attract diverse credit offerings. This would transform two isolated price points into the nascent stages of a genuine on-chain yield curve.

-

Publication and independent audit of the orderbook contracts: This step is paramount for building institutional trust, mitigating smart contract risk, and demonstrating a commitment to transparency and security.

-

Integration by a downstream lender: If a prominent DeFi lending protocol were to list an Agra-traded token as collateral, with its underwriting explicitly citing the on-chain market price (rather than just the NAV), it would validate Agra’s effectiveness as a price discovery mechanism.

None of these milestones are guaranteed, but all are within the reachable path for the product as it stands today. The dynamic nature of beta venues means that fundamental aspects like NAVs, coupons, book depth, and market addresses are point-in-time snapshots from late April 2026. The live state, and the evolution of these critical indicators, can be tracked directly on bonds.agra.gg, where every material development has the potential to reshape the landscape of tokenized private credit.

{kind=link}