The landscape of homeownership, long considered a bedrock of financial security and generational wealth, is becoming increasingly challenging, particularly for younger demographics. Faced with a confluence of escalating interest rates, soaring property values, and a persistent construction deficit, prospective homebuyers are encountering significant hurdles. Adding to this complexity are outdated and inefficient lending practices characterized by bloated sales teams, manual processing, and legacy technology. These inefficiencies translate into substantial overhead costs, which are ultimately borne by borrowers through elevated interest rates and, according to recent studies, billions in excess fees annually. This situation further exacerbates the affordability crisis, pushing the dream of homeownership further out of reach for many.

In response to these persistent challenges, Wealthfront Home Lending has officially launched, aiming to revolutionize the mortgage process by applying the same technological innovation that transformed the investment and cash management sectors. Wealthfront, a prominent fintech company known for its client-centric approach and fee-reduction strategies, is now extending its mission to democratize access to homeownership. The company’s strategy centers on building a fully digital mortgage product, streamlining operational workflows, and automating away the costly overhead inherent in traditional lending institutions. This digital-first approach is designed to consistently offer mortgage rates that are at least 0.50% below the national average, coupled with an enhanced client experience.

This strategic move into home lending comes as a direct response to years of client requests for a "Wealthfront version" of the mortgage process. Many existing Wealthfront clients already utilize the platform for saving towards a down payment, collectively holding an estimated $116 billion in real estate. In 2025 alone, Wealthfront facilitated $2.3 billion in down payment wires, underscoring the significant financial commitments its clients are making toward homeownership. By integrating the mortgage application and servicing process onto the same platform, Wealthfront aims to provide a seamless financial management experience for its digitally native clientele as they navigate this significant life milestone.

Significant Savings Through Technological Efficiency

A core tenet of Wealthfront Home Lending’s offering is the promise of substantial financial savings for borrowers. Affordability remains the paramount concern for individuals navigating the current real estate market. Mortgage rates not only dictate a buyer’s initial entry into homeownership but also profoundly impact their long-term financial health over the life of the loan. Wealthfront posits that by leveraging advanced technology to automate the labor-intensive processes common in traditional mortgage firms, they can offer rates consistently below the national average.

As of March 31, 2026, for the average new home purchaser, a rate difference of 0.50% or more translates into an estimated savings of approximately $70,000 over the life of a 30-year mortgage. This significant reduction in interest costs frees up capital that borrowers can then reallocate towards other critical long-term financial goals, such as investments, retirement savings, or further wealth accumulation. This approach aligns with Wealthfront’s broader philosophy of empowering clients to maximize their financial potential by minimizing unnecessary costs and optimizing returns.

Transparent Pricing and an Unwavering Commitment to Honesty

Beyond competitive interest rates, Wealthfront Home Lending is prioritizing transparent and straightforward pricing, aiming to eliminate the "bait-and-switch" tactics that have plagued the industry. Prospective borrowers will encounter clear, easily understandable rate information directly within the platform. Wealthfront’s integrated rate calculator provides personalized and immediate estimates for both new homebuyers and those looking to refinance, fostering confidence and enabling informed decision-making.

A key differentiator in Wealthfront’s pricing model is its upfront, flat underwriting fee of $999. Traditional lenders often embed this cost within a percentage of the total loan amount, typically ranging from 0.5% to 1%. For a $500,000 loan, this could amount to $2,500 to $5,000 in hidden fees. Wealthfront’s transparent, flat fee simplifies the budgeting process for borrowers and eliminates the ambiguity associated with hidden charges. This commitment to upfront honesty aims to build trust and provide a predictable financial framework for clients.

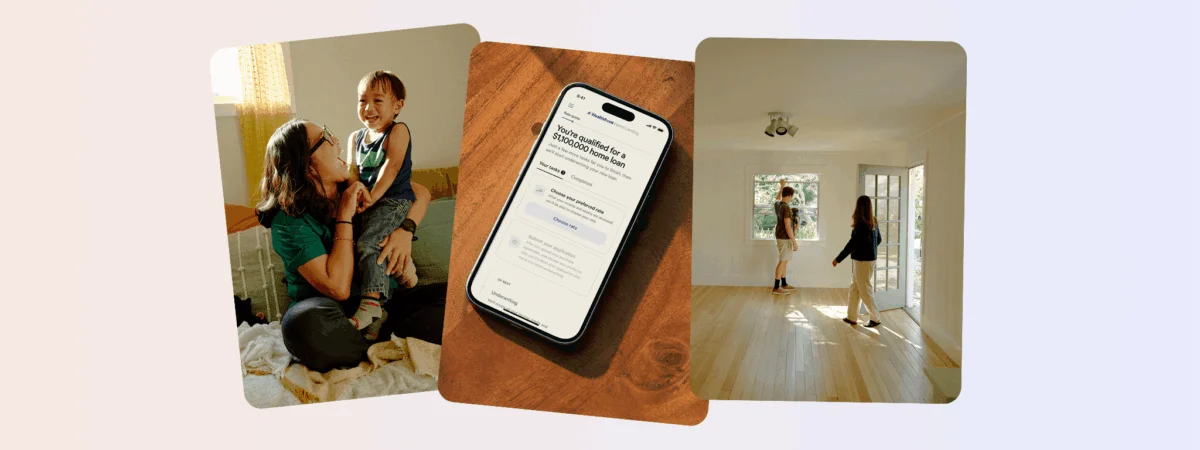

A Mortgage Experience Tailored for the Digital Age

Wealthfront Home Lending is distinguished by its ambition to create the first mortgage product entirely manageable from a smartphone. The platform features a self-serve application process, allowing clients to proceed at their own pace while providing real-time tracking of their loan status. This digital-first approach is complemented by a team of experienced loan officers and licensed industry professionals who are readily available via phone and email.

The integration of client financial data already held by Wealthfront, including linked account information and verified income, is expected to significantly reduce the need for manual document compilation. This data synergy streamlines the underwriting process and further enhances efficiency. Looking ahead, Wealthfront plans to introduce additional innovative features, such as a rapid pre-approval process and personalized in-app decision support tools. These tools will assist clients in selecting the most suitable mortgage, evaluating the impact of discount points, and making other crucial financial decisions. Furthermore, the company is developing a "one-click" refinancing experience for clients with linked mortgages, simplifying the process of securing lower interest rates with minimal effort.

The Evolution of Wealthfront’s Financial Ecosystem

Since its inception, Wealthfront has been dedicated to leveraging technology to improve financial outcomes and deliver tangible value to its clients. The company’s journey began with revolutionizing the investment management space, where it has demonstrably saved clients an estimated $1.5 billion in advisory fees compared to traditional 1% fee models. Furthermore, its sophisticated Tax-Loss Harvesting strategy is credited with saving investing clients an estimated $1.3 billion in taxes. The subsequent expansion into cash management saw the development of a Cash Account that has paid out over $4.7 billion in interest from program banks since its introduction. The current foray into home lending marks a significant expansion, addressing what is often the most substantial financial transaction in a client’s life.

Wealthfront’s established profitability provides a crucial advantage, freeing the company from the pressure of meeting aggressive mortgage quotas for survival. This financial stability allows Wealthfront Home Lending to prioritize the development of a superior product and maintain competitive rates. It also enables the company to offer unbiased guidance that is genuinely in the best interest of its clients, rather than being driven by internal sales targets.

The Road Ahead for Wealthfront Home Lending

While Wealthfront Home Lending is still in its nascent stages, the company has ambitious plans for its future. Having already secured licensing in 26 states, Wealthfront is implementing a phased rollout strategy to ensure an exceptional client experience. Currently, its mortgage offering is fully operational in Colorado, with planned expansions into Texas, California, and additional states in the near future. Prospective clients are encouraged to visit the Wealthfront Home Lending website to learn more about the product and view current rates.

The expansion into home lending represents a significant step in Wealthfront’s mission to provide a comprehensive suite of financial services designed to help individuals build and manage their wealth effectively. By integrating investing, cash management, and now home financing onto a single, intuitive platform, Wealthfront aims to become a central financial partner for its clients throughout their lives. This holistic approach simplifies financial management and empowers users to make more informed decisions across all aspects of their financial lives. The company’s commitment to technological innovation and client advocacy positions it to disrupt the traditional mortgage market, offering a more accessible, affordable, and user-friendly experience for a new generation of homeowners.

Disclosure

All mortgage products are offered by Wealthfront Home Lending, LLC NMLS 2358115. Home loan availability is subject to credit approval and applicable state and federal licensing requirements. Rates vary based on credit profile, loan terms, and market conditions. Not all applicants will qualify for the lowest advertised rates. This communication is for informational purposes only and does not constitute a solicitation for a loan or an offer to lend or extend credit. Equal Housing Opportunity. Wealthfront Home Lending, LLC is an affiliate of Wealthfront Advisers LLC, an SEC-registered investment adviser, Wealthfront Brokerage LLC, Member FINRA/SIPC, Wealthfront Software LLC, Wealthfront Strategies LLC, and the Wealthfront Corporation. The information contained in this communication is provided for general informational purposes only, and should not be construed as investment, tax, or home lending advice. Interest rates and loan terms reflected are for illustrative purposes only and do not constitute a solicitation for a loan or an offer to lend or extend credit. This is not a commitment to lend. Any links provided to other server sites are offered as a matter of convenience and are not intended to imply that Wealthfront Corporation or its affiliates endorse, sponsor, promote and/or is affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

*Rate comparison based on Freddie Mac Primary Mortgage Market Survey® average for 30-year fixed-rate mortgages as of April 6, 2026. Rate available to qualified borrowers meeting the following criteria: 780+ FICO score, $750,000 purchase price, primary single-family residence in Austin, TX, 20% down payment, and payment of 1 discount point. Actual rates may vary. APR and additional terms apply. Not all borrowers will qualify.

Fee Savings Methodology: We first estimated the hypothetical fee a traditional advisor would charge by assuming a 1% advisory fee on assets under management (AUM). This was calculated by taking our total daily cumulative investing AUM across our managed advisory products and multiplying it by the daily effective fee (0.01 / 365) to get the hypothetical total fee amount. Next, we calculated the total fees actually charged by Wealthfront across these managed products, net of any fee waivers. Note: Standalone Direct Indexing accounts were excluded from this analysis because the appropriate comparison is typically the expense ratio of an ETF, not the advisory fee. Similarly, Stock Investing Account and our Automated Bond Ladder were also excluded as their relevant point of comparison is generally not a 1% advisory fee account. The difference between the hypothetical traditional adviser total fees and the actual Wealthfront fees charged for managed advisory products is the estimated client fee savings. This is provided for illustrative purposes only. Actual results or experiences will vary.

Estimated tax savings: We calculated the estimated tax savings based on our clients’ current self-reported income, state of residence, and tax-filing status. From that, we inferred a combined federal and state tax rate (if applicable) for each client. We then multiplied each client’s rate by their harvested losses and added those numbers up to get the $1.3B in estimated tax savings since inception (01/2012) through 02/15/2026. This calculation also assumes that there are enough capital gains to be fully offset by the harvested losses and that current tax laws and rates remain in effect. The actual tax savings realized by any individual client will vary based on their specific tax situation, investment activity, and market performance. These figures are an estimate of potential tax benefits and are not guaranteed. Investors should consult with a tax professional regarding their specific circumstances.

Interest paid out: The total interest figure represents the total amount of interest received by the Cash Account owners over the lifetime of all currently active Cash Accounts. Includes data from 02/14/2019- 02/15/2026. Interest is paid from program banks. The Cash Account, which is not a deposit account, is offered by Wealthfront Brokerage LLC (“Wealthfront Brokerage”), Member FINRA/SIPC. Wealthfront Brokerage is not a bank.

About the author(s)

David Fortunato is Wealthfront’s Chief Executive Officer. He joined Wealthfront in 2009 as the company’s inaugural CTO and was instrumental in launching the company to its first clients in 2011. Previously to his role as CEO, David was the President of Wealthfront. David holds a BS in computer science and economics from Amherst College. View all posts by David Fortunato.

{kind=link}