When individuals engage with Betterment, the digital investment platform, they are empowered to establish specific savings objectives, each meticulously mapped to a defined time horizon and intended purpose. This robust goal-setting framework allows for the creation of virtually unlimited investment goals, providing users with a personalized roadmap for their financial aspirations. Upon initiating a new investment goal, users are prompted to specify the anticipated timeframe for its realization and to categorize it among a suite of predefined goal types. These categories are designed to align investment strategies with the unique liquidity needs and risk profiles associated with each financial objective.

Beyond traditional investment goals, Betterment extends its capabilities to encompass cash management through its Cash Reserve offering and speculative investments via its Crypto ETF portfolio. However, the allocation methodologies discussed herein are specifically tailored for conventional investment goals and do not extend to these specialized offerings.

For the vast majority of investment goals, with the singular exception of Emergency Funds, the interplay between the anticipated time horizon and the selected goal type critically informs Betterment’s strategic allocation recommendations. This data allows the platform to infer when the funds are likely to be accessed and the intended withdrawal pattern—whether it be a singular, immediate liquidation for a significant purchase or a series of periodic withdrawals, as is common for retirement income strategies. Emergency Funds, by their very nature, are exempt from a predefined time horizon. While Betterment may assign a provisional timeframe for the purpose of initial savings and deposit guidance, this designation does not influence the recommended investment allocation. This is fundamentally because the timing and magnitude of unforeseen emergency expenses are inherently unpredictable. It is worth noting that Betterment maintains a modest allocation of operational cash within automated investment portfolios across taxable accounts, health savings accounts, and individual retirement accounts, a detail further elaborated in the platform’s disclosures.

The core of Betterment’s investment allocation advisory lies in its sophisticated modeling. For all goals, excluding Emergency Funds, the platform crafts recommended investment allocations by projecting a spectrum of potential market outcomes. From this probabilistic analysis, it identifies and averages the risk levels that have historically delivered the most favorable performance within the 5th to 50th percentile range of outcomes. For Emergency Funds, the objective shifts towards balancing growth potential with a stringent limitation on the risk of drawdowns that might exceed a predefined buffer above the essential emergency sum.

Tailored Investment Allocations: A Spectrum of Risk and Reward

The following table outlines the recommended investment allocation ranges for various goal types, excluding Emergency Funds, illustrating the strategic adjustments made based on temporal and functional parameters:

| Goal Type | Most Aggressive Recommended Allocation | Most Conservative Recommended Allocation |

|---|---|---|

| Major Purchase | 90% stocks (33+ years) | 0% stocks (time horizon reached) |

| Education | 90% stocks (33+ years) | 0% stocks (time horizon reached) |

| Retirement | 90% stocks (20+ years until retirement age) | 56% stocks (retirement age reached) |

| Retirement Income | 56% stocks (24+ years remaining life expectancy) | 30% stocks (9 years or less remaining life expectancy) |

| General Investing | 90% stocks (20+ years) | 56% stocks (time horizon reached) |

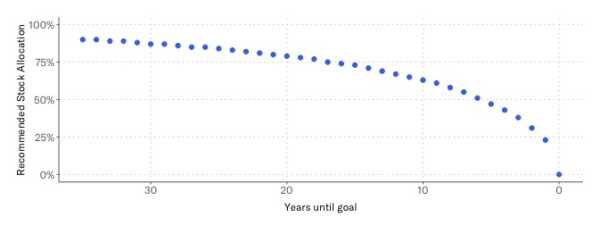

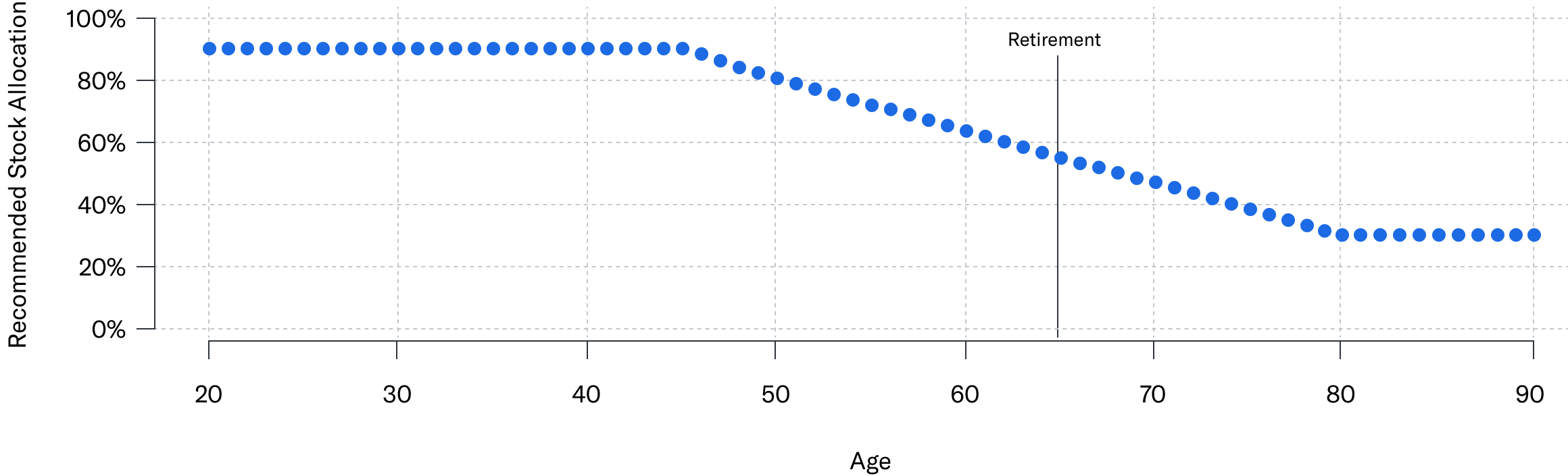

A clear trend emerges from this data: the longer the time horizon of an investment goal, the more aggressive Betterment’s recommended allocation tends to be. Conversely, shorter time horizons necessitate a more conservative approach. This dynamic adjustment process is colloquially referred to as a "glidepath," representing the systematic evolution of the recommended allocation for a specific goal over time.

The Evolution of Investment Strategies: Glidepaths in Action

Betterment provides detailed glidepaths for its various goal types, visually representing the strategic shifts in asset allocation as a goal approaches its target date.

Major Purchase and Education Goals: These goals typically exhibit a pronounced downward trajectory in stock allocation as the target date nears. For instance, a "Major Purchase" goal with a very distant horizon might begin with an aggressive 90% allocation to stocks. As the years tick by, this allocation gradually decreases, becoming increasingly conservative to preserve capital as the purchase date looms. The objective is to minimize the risk of market downturns impacting the funds needed for the significant expenditure.

Retirement and Retirement Income Goals: The glidepaths for retirement are more nuanced, reflecting the extended nature of these goals and the potential for ongoing income generation post-retirement. For a "Retirement" goal, an aggressive allocation might be maintained for decades leading up to retirement age, aiming for substantial long-term growth. Upon reaching retirement age, the allocation becomes more conservative, typically shifting towards a higher percentage of bonds to provide stability and income. The "Retirement Income" goal introduces further complexity, accounting for projected life expectancy. Here, the allocation adjusts based on the remaining years of anticipated income needs, moving from a more growth-oriented strategy to a more capital-preservation-focused one as the individual approaches the latter stages of their expected lifespan.

General Investing Goals: These goals, often characterized by a longer-term outlook and less immediate liquidity needs, follow a glidepath that balances growth with capital preservation. While they can start with aggressive allocations, they tend to become more conservative as the investor approaches their self-defined time horizon, ensuring that accumulated gains are protected.

Auto-Adjust: Proactive Risk Management for Goal Achievement

A key feature within Betterment’s offering is the "auto-adjust" functionality. This intelligent system automatically calibrates a goal’s allocation to manage risk effectively, progressively shifting towards a more conservative stance as the investment timeline nears its conclusion. The adjustments are made incrementally, ensuring a smooth and predictable glidepath.

The specific parameters of auto-adjust vary across goal types. For "Major Purchase" and "Education" goals, the glidepath is notably more conservative, especially for short time horizons. This reflects the expectation of a full liquidation of the investment upon reaching the target date, necessitating a high degree of capital preservation. In contrast, retirement goals, which anticipate distributions over an extended period, are designed to maintain a higher risk allocation even as the target retirement age is reached, facilitating continued growth and income generation.

The auto-adjust feature is available for investment goals with an associated time horizon, with exceptions for Emergency Fund goals, the Target Income portfolio, and the Goldman Sachs Tax-Smart Bonds portfolio. It is compatible with several of Betterment’s core portfolio options, including the Betterment Core portfolio, SRI portfolios, Innovation Technology portfolio, Value Tilt portfolio, and the Goldman Sachs Smart Beta portfolio. When opting for Betterment’s recommended allocation, users have the choice to enable auto-adjust. This feature employs a combination of reactive and proactive rebalancing techniques to ensure the goal’s allocation remains aligned with the platform’s recommended glidepath.

Beyond Risk Capacity: Integrating Personal Risk Tolerance

While Betterment’s recommended allocations and glidepaths are grounded in the concept of "risk capacity"—the ability of a goal to withstand financial setbacks based on its time horizon and liquidation strategy—the platform recognizes that individual investors may have different comfort levels with risk. Consequently, clients are provided with the autonomy to either accept these recommendations or to diverge from them based on their personal risk tolerance.

To facilitate this personalized approach, Betterment employs an intuitive interactive slider. This tool allows users to dynamically adjust their asset allocation, specifically toggling between the proportion of stocks and bonds, until they identify an allocation that aligns with their expected growth outcomes and their willingness to accept potential fluctuations. This slider categorizes risk tolerance into five distinct levels, empowering users to fine-tune their investment strategy beyond the platform’s baseline recommendations. This integration of risk capacity and personal risk tolerance creates a truly customized investment experience, ensuring that each user’s financial journey is aligned with both their objective reality and their subjective comfort with market volatility.

The implications of this dynamic approach are far-reaching. By offering tailored glidepaths and the flexibility to adjust for individual risk tolerance, Betterment aims to democratize sophisticated investment management, making it accessible and understandable for a broad range of investors. This strategy is designed not only to optimize potential returns but also to mitigate undue stress and anxiety associated with market fluctuations, fostering a more sustainable and successful long-term investment experience. The platform’s commitment to data-driven recommendations, coupled with user empowerment, positions it as a significant player in the evolving landscape of digital wealth management.

{kind=link}