Betterment, a leading digital investment advisor, has detailed its sophisticated approach to personalized investment allocation, emphasizing how it dynamically adjusts portfolio strategies based on individual financial goals, time horizons, and risk tolerance. This nuanced methodology aims to optimize potential growth while mitigating risk, offering clients a clear path toward achieving their long-term financial objectives, from major purchases and education funding to retirement and general wealth accumulation. The firm’s strategy underscores a departure from one-size-fits-all investment plans, instead favoring a data-driven and goal-centric model that adapts over time.

The Foundation of Goal-Based Investing

At its core, Betterment’s investment philosophy is built around the concept of goal-based investing. Upon signing up, users are prompted to establish specific financial goals. This process involves defining the anticipated timeframe for achieving each goal and selecting a corresponding goal type. Betterment supports a virtually unlimited number of investment goals, each treated as a distinct savings and investment vehicle. While the platform offers specialized solutions for cash (Cash Reserve) and cryptocurrency (Crypto ETF portfolio), these are outside the scope of the allocation methodology being discussed.

For all standard investment goals, except for emergency funds, the interplay between the anticipated time horizon and the chosen goal type is crucial. This information informs Betterment about when the client plans to access the funds and how they intend to withdraw them. For instance, a goal intended for a major purchase might anticipate a lump-sum, immediate liquidation, whereas a retirement goal would likely involve periodic withdrawals over an extended period.

Navigating the Nuances of Emergency Funds

Emergency Funds represent a unique category within Betterment’s framework. By their very nature, these funds lack a predetermined time horizon, as unforeseen expenses can arise at any moment. While Betterment may assign a provisional time horizon to facilitate initial saving and deposit advice, this does not influence the recommended investment allocation for the emergency fund itself. This is a deliberate design choice, acknowledging the unpredictability of emergencies and the need to prioritize capital preservation and accessibility. Betterment maintains a modest operational cash allocation within automated investing portfolios across taxable, health savings, and individual retirement accounts to address immediate needs. Further details on this are available in the respective portfolio disclosures.

Tailored Allocations: The Role of Time Horizon and Goal Type

For all investment goals, with the exception of Emergency Funds, Betterment crafts a recommended investment allocation that is directly influenced by the user’s specified time horizon and goal type. This allocation is not arbitrary; it is derived from sophisticated modeling that projects a spectrum of potential market outcomes. The resulting recommendation averages the performance of the most successful risk levels across the 5th to 50th percentiles of these projections.

For Emergency Funds, the allocation strategy shifts. It is designed to offer a degree of growth potential while strictly limiting the risk of drawdowns that could significantly deplete the fund below the essential buffer required for unexpected expenses.

The "Glidepath": A Dynamic Investment Journey

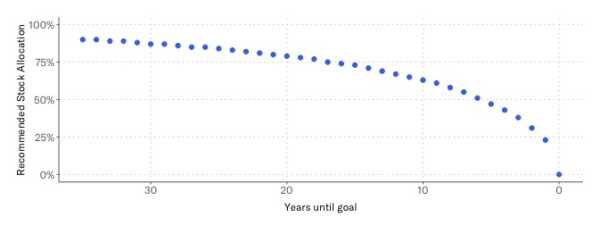

The cornerstone of Betterment’s allocation strategy for most investment goals is the concept of a "glidepath." This refers to the systematic adjustment of an investment portfolio’s asset allocation over time, moving from more aggressive to more conservative as the goal’s deadline approaches. This principle is vividly illustrated in the table below, which outlines the ranges of recommended investment allocations for various goal types, excluding Emergency Funds:

| Goal Type | Most Aggressive Recommended Allocation | Most Conservative Recommended Allocation |

|---|---|---|

| Major Purchase | 90% stocks (33+ years) | 0% stocks (time horizon reached) |

| Education | 90% stocks (33+ years) | 0% stocks (time horizon reached) |

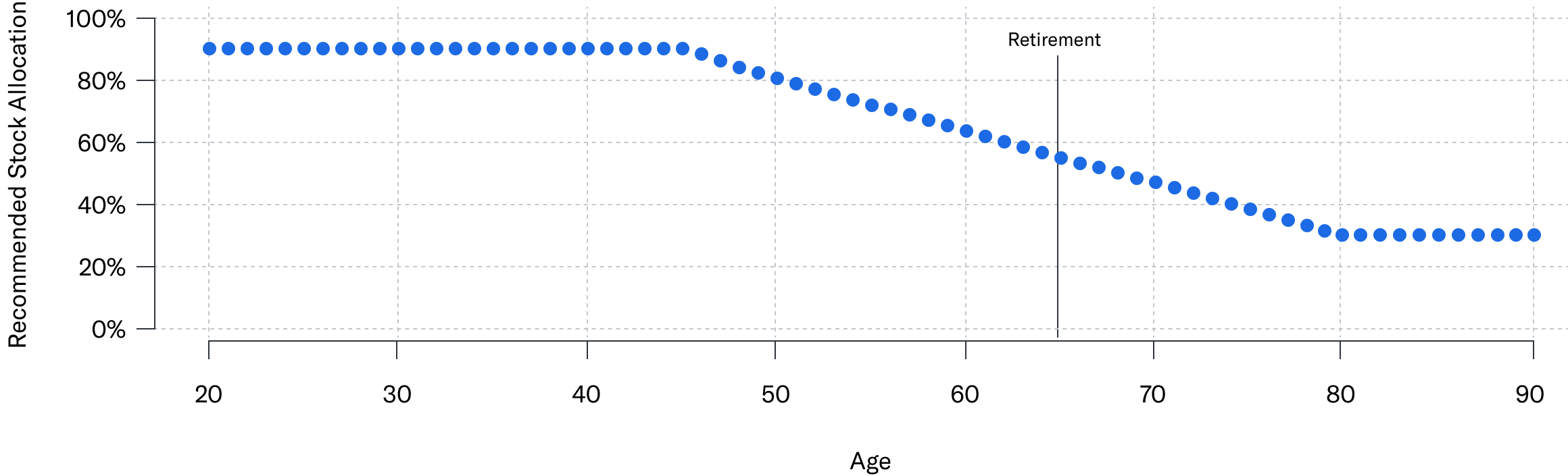

| Retirement | 90% stocks (20+ years until retirement age) | 56% stocks (retirement age reached) |

| Retirement Income | 56% stocks (24+ years remaining life expectancy) | 30% stocks (9 years or less remaining life expectancy) |

| General Investing | 90% stocks (20+ years) | 56% stocks (time horizon reached) |

The data clearly indicates a fundamental principle: the longer the time horizon for a goal, the more aggressive Betterment’s recommended allocation tends to be. Conversely, shorter time horizons lead to more conservative recommendations. This adaptive strategy ensures that investments are positioned to capture potential market growth during the early stages of a long-term goal, while gradually de-risking as the need for the funds draws nearer, thereby protecting accumulated capital.

Visualizing the Glidepath: Strategic Adjustments Over Time

Betterment provides visual representations of these glidepaths for its key goal types:

Major Purchase/Education Goals: For goals such as purchasing a home or funding education, the glidepath typically starts with a high allocation to stocks, often up to 90%, for very long time horizons (33+ years). As the target date approaches, the allocation progressively shifts towards a more conservative mix, eventually reaching 0% stocks at the time the horizon is reached, indicating a full liquidation strategy.

Retirement/Retirement Income Goals: Retirement planning involves a more sustained period of risk-taking, given the extended nature of retirement and the potential for income generation over decades. For individuals planning to retire in 20 or more years, the allocation can be as high as 90% stocks. Upon reaching retirement age, the allocation typically adjusts to around 56% stocks. For those in Retirement Income phases, the strategy is further refined based on remaining life expectancy, with allocations ranging from 56% stocks for those with over 24 years of life expectancy to 30% stocks for those with 9 years or less. A hypothetical example for a client retiring at 65 and living to 90 illustrates a gradual decrease in stock allocation as life expectancy shortens, but a continued presence in equities to support long-term income needs. It is important to note that such examples do not represent actual client performance and are not indicative of future results, as actual outcomes are subject to numerous variables, including market fluctuations and individual account activity.

General Investing Goals: This category, designed for broader wealth accumulation without a specific immediate objective, mirrors the retirement glidepath in its initial aggressive stance for longer time horizons (20+ years). It also becomes more conservative as the time horizon is reached, typically settling at around 56% stocks.

The "Auto-Adjust" Feature: Seamless Risk Management

To facilitate the smooth execution of these glidepaths, Betterment offers an "auto-adjust" feature. This automated system continuously manages a goal’s allocation, gradually reducing risk as the investing timeline nears its end. The adjustments are made incrementally, creating a seamless transition.

The auto-adjust feature is available for investing goals with a defined time horizon, excluding Emergency Funds, the Target Income portfolio (developed with BlackRock), and the Goldman Sachs Tax-Smart Bonds portfolio. It is applicable to Betterment’s Core portfolio, SRI portfolios, Innovation Technology portfolio, Value Tilt portfolio, and the Goldman Sachs Smart Beta portfolio. By enabling this feature during the acceptance of recommended allocations, clients empower Betterment to proactively and reactively rebalance their portfolios, ensuring they remain aligned with the desired glidepath.

This dynamic approach is particularly evident when comparing different goal types. For instance, "Major Purchase" goals adopt a more conservative trajectory than "Retirement" or "General Investing" goals, especially for short time horizons. This is because the expectation for a major purchase is often a complete withdrawal of funds at a specific date. In contrast, retirement goals anticipate ongoing distributions, justifying a higher risk allocation even as retirement age is reached, to sustain income over an extended period.

Adjusting for Personal Risk Tolerance: Beyond "Risk Capacity"

While the recommended allocations and glidepaths are primarily based on "risk capacity" – the ability of a goal to withstand financial setbacks based on its timeframe and liquidation strategy – Betterment recognizes that individual comfort levels with risk can vary significantly. Clients are given the autonomy to accept these recommendations or to deviate from them.

To empower this personal adjustment, Betterment employs an interactive slider. This tool allows clients to intuitively adjust the allocation between stocks and bonds, visualizing the potential range of growth outcomes associated with different risk levels. This empowers users to select an allocation that aligns with their personal comfort zone for risk, ensuring they feel confident and in control of their investment journey. Betterment categorizes risk tolerance into five distinct levels, providing a structured framework for clients to navigate their choices.

Supporting Data and Market Context

The efficacy of Betterment’s goal-based allocation strategy is underpinned by extensive financial research and historical market data. Studies consistently show that for long-term investment horizons, higher allocations to equities generally yield superior returns compared to more conservative asset mixes. For example, historical data from the S&P 500 index, a common benchmark for U.S. stock market performance, has demonstrated average annual returns of approximately 10-12% over extended periods. However, this comes with greater volatility. Conversely, fixed-income investments, such as bonds, offer lower potential returns but also significantly reduced volatility, making them suitable for shorter-term goals or for investors with a low risk tolerance.

The concept of a glidepath is widely adopted in retirement planning, particularly by target-date funds. These funds automatically adjust their asset allocation to become more conservative as the target retirement date approaches. Betterment’s approach refines this concept by integrating it with a broader spectrum of financial goals, not just retirement, and offering greater transparency and user control through its platform.

Broader Implications for the Investment Landscape

Betterment’s emphasis on personalized, goal-driven investment allocation signals a broader trend in the financial services industry. As consumers become more financially literate and demand greater personalization, robo-advisors and traditional financial institutions are increasingly moving away from standardized investment products towards tailored solutions. This shift is driven by the understanding that financial success is not solely determined by market performance, but also by an investor’s ability to stay invested through market cycles, which is often facilitated by an allocation strategy that aligns with their comfort level and financial objectives.

The ability to set multiple, distinct goals, each with its own investment strategy and glidepath, allows individuals to manage their finances more holistically. This approach can help prevent the premature liquidation of long-term investments to fund short-term needs, thereby enhancing the likelihood of achieving all financial objectives. Furthermore, the transparency provided by platforms like Betterment, in explaining the rationale behind allocation recommendations and offering tools for customization, empowers investors and fosters greater confidence in their financial planning. This sophisticated yet accessible methodology represents a significant advancement in democratizing sophisticated investment strategies for a wider audience.

{kind=link}