The European venture capital landscape is undergoing a significant transformation, evidenced by the monumental $1.8 billion Series E funding round secured by Munich-based defense technology firm Helsing. This infusion of capital, which values the company at an impressive $18 billion, not only establishes a new record for the largest private defense tech funding round in European history but also underscores a broader trend of increased investor appetite for companies operating within the defense sector. Helsing’s total funding now stands at a substantial $3.3 billion, reflecting a robust trajectory of growth and investor confidence.

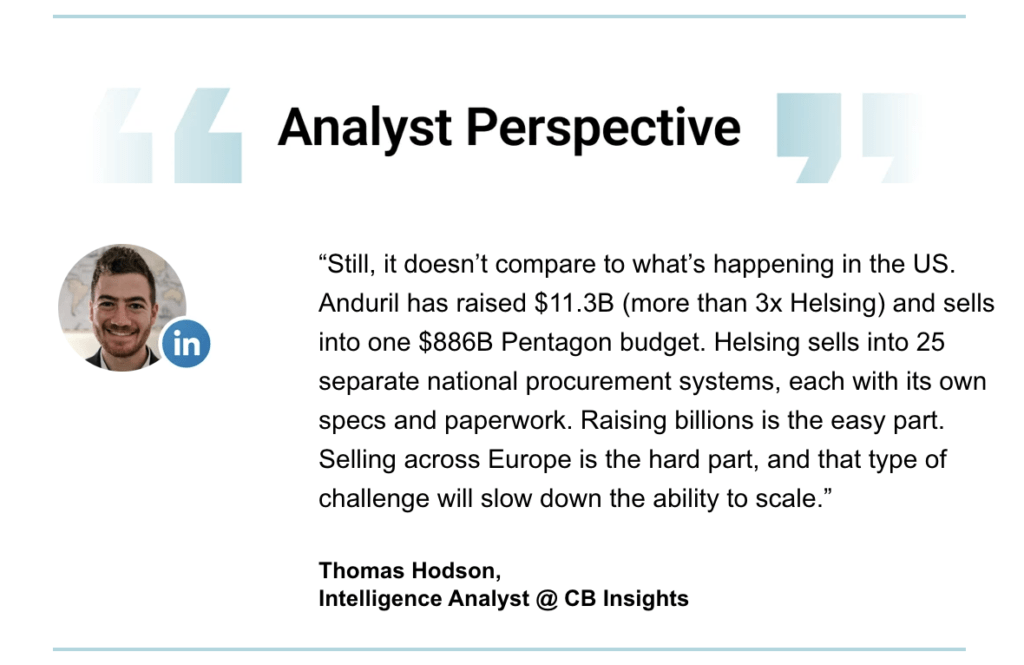

The sheer magnitude of this funding round, however, is only one part of the compelling narrative. Experts suggest that the strategic value Helsing places on its ability to navigate the intricate and often fragmented procurement systems across 25 different European nations may have been a more significant factor in attracting such substantial investment than the capital itself. This approach differentiates Helsing from many other technology companies that might prioritize a singular, large-scale funding event. Instead, Helsing appears to be building a sustainable growth model rooted in its deep understanding of governmental acquisition processes, which are notoriously complex and vary significantly from one country to another.

This achievement is particularly noteworthy when viewed against the backdrop of the European venture capital market’s historical hesitancy towards defense investments. Just five years ago, many European venture capital firms actively excluded defense technology from their portfolios. This aversion was largely attributed to a confluence of factors, including stringent ESG (Environmental, Social, and Governance) mandates, limitations imposed by limited partners (LPs), and a prevailing cultural sentiment that associated proximity to defense systems with reputational risk. The landscape, however, has demonstrably shifted.

The Evolving European Defense Tech Investment Climate

The recent surge in funding for European defense tech startups is a clear indicator of this evolving sentiment. In 2025 alone, these companies collectively raised $3.2 billion, representing a significant 37% year-over-year increase. This figure is also approximately three times the amount raised just five years prior, painting a picture of a sector that is rapidly gaining traction and investor interest. Furthermore, the number of unique investors participating in European defense rounds has nearly tripled since 2020, signaling a broadening base of support and a growing recognition of the sector’s potential.

This shift can be attributed to a confluence of geopolitical realities and a recalibration of investment strategies. Heightened global tensions and a renewed focus on national security have prompted governments across Europe to increase defense spending. This, in turn, has created a more fertile ground for innovation and investment in companies that can provide cutting-edge solutions to meet these evolving needs. Venture capitalists, once wary, are now recognizing the strategic importance and long-term viability of the defense technology sector.

Helsing’s Strategic Advantage: Mastering Procurement

Helsing’s success is deeply intertwined with its operational strategy, which emphasizes adaptability and integration across diverse national defense infrastructures. The company’s focus on navigating 25 distinct procurement systems implies a sophisticated understanding of bureaucratic processes, regulatory frameworks, and the specific technological requirements of various European armed forces. This capability is not merely a logistical challenge; it is a core competitive advantage.

For defense ministries, procuring new technologies is a lengthy and often arduous process. The ability of a company like Helsing to streamline this process, offer solutions that meet a range of national specifications, and build trust across multiple governments is invaluable. This approach reduces the friction in sales cycles and fosters deeper, more enduring relationships with national defense establishments. It suggests a business model that is less reliant on a single, massive government contract and more focused on building a distributed network of engaged clients, thereby mitigating risk and ensuring a more stable revenue stream.

Broader Market Trends and Investor Insights

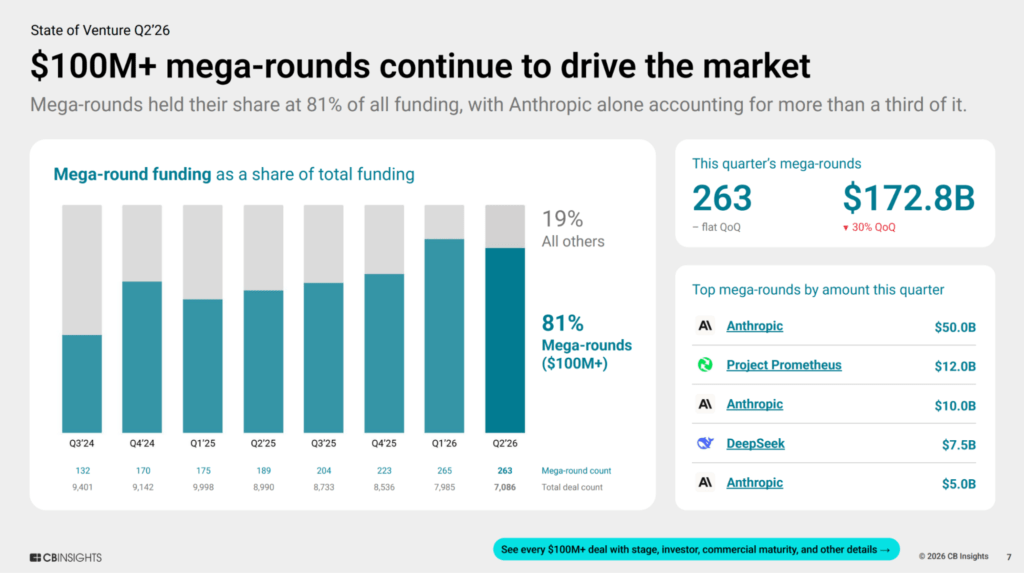

The record-breaking funding round for Helsing is occurring within a broader context of significant shifts in the global venture capital market, particularly in the second quarter of 2026. While the quarter saw robust overall funding, reaching $212.9 billion—the second-highest on record—a significant portion of this capital was concentrated in a few mega-rounds. Notably, AI company Anthropic alone accounted for over a third of all mega-round funding, with a $65 billion valuation. This trend of concentration, driven by a few exceptionally large deals, presents both opportunities and challenges for the broader venture ecosystem.

The Q2 2026 data reveals that mega-rounds, deals exceeding $100 million, captured an astounding 81% of total funding. This mirrors the trend observed in the previous quarter, which was heavily influenced by substantial investments in both Anthropic and OpenAI. However, the Q2 reliance on Anthropic as a singular driver highlights a potential vulnerability in the market’s reliance on a few dominant players. While this concentration can fuel rapid advancements in specific fields, it also means that the performance of the broader market can be disproportionately affected by the success or failure of these few entities.

In contrast to the mega-round dominance, the overall deal count in Q2 2026 reached a decade low, and exit values have declined for two consecutive quarters. This indicates a tightening market for smaller rounds and a more challenging environment for initial public offerings (IPOs) and acquisitions. The data suggests a bifurcated market: one segment characterized by massive capital infusions into a select few, and another segment facing reduced deal flow and exit opportunities.

The Role of Data and Strategic Intelligence

CB Insights, a leading provider of data and analytics on emerging technology and venture capital, has been at the forefront of analyzing these trends. Their research, including the "State of Venture" report, provides critical insights into the dynamics shaping the investment landscape. The firm’s partnership with HLTH USA for the 2026 event further illustrates the growing importance of data-driven strategic intelligence.

The launch of the "Insights Hub" in collaboration with HLTH USA exemplifies this commitment. This interactive dashboard, powered by CB Insights’ extensive data on over 12,250 attendees, aims to transform networking at major industry events. By providing attendees with data-driven insights into companies and trends, the Hub enables more targeted and productive connections, moving beyond serendipitous encounters on the trade show floor. This approach highlights the increasing demand for tools that can help navigate complex ecosystems and identify strategic opportunities, a principle that resonates strongly with Helsing’s own operational philosophy.

Analysis and Implications

Helsing’s record-breaking funding round is more than just a financial milestone; it is a bellwether for several critical developments. Firstly, it signals a significant de-risking of defense technology as an investment category in Europe. The continued geopolitical instability and the clear need for advanced defense capabilities have compelled investors to reassess their positions, recognizing that national security is a persistent and growing market.

Secondly, Helsing’s success underscores the strategic advantage of deep domain expertise, particularly in navigating complex governmental procurement processes. Companies that can demonstrate an ability to understand and adapt to the unique requirements of different national defense agencies are likely to command significant investor attention. This is particularly relevant in sectors where long sales cycles and regulatory hurdles are standard.

Thirdly, the contrasting trends in the broader venture market – the dominance of mega-rounds alongside a decline in deal count and exits – suggest a maturing and consolidating market. Investors are increasingly focusing their capital on companies with proven traction and clear pathways to significant scale, particularly those addressing large, systemic needs like national security.

The implications for the defense technology sector are profound. We can expect to see continued investment in companies that offer innovative solutions in areas such as artificial intelligence, cybersecurity, unmanned systems, and advanced materials. The ability to integrate these technologies into existing military platforms and to navigate the procurement processes of multiple allied nations will be key differentiators.

Furthermore, the success of Helsing may encourage other European startups in related fields to pursue aggressive growth strategies and seek substantial funding. The perception of defense tech as a viable and lucrative investment area is likely to grow, potentially leading to a more dynamic and competitive European defense innovation ecosystem. As the geopolitical landscape continues to evolve, the strategic importance of companies like Helsing, which are adept at bridging technological innovation with national security needs, will only increase. Their approach to scaling across diverse procurement systems offers a compelling model for future growth in a sector vital to global stability.

{kind=link}