When individuals embark on their investment journeys with Betterment, a core feature allows them to meticulously define and pursue specific financial objectives. This robust platform empowers users to establish an unlimited number of investment goals, each tailored to a distinct purpose and timeline. During the creation of a new investment goal, users are prompted to provide an anticipated time horizon, which is the projected duration until the funds will be needed. Crucially, they also select a specific goal type. These goal types, fundamental to Betterment’s allocation methodology, dictate how investment strategies are formulated to align with the user’s financial aspirations and the inherent risks associated with different investment horizons.

While the primary focus of Betterment’s allocation advice centers on traditional investment goals, the platform also extends its capabilities to encompass cash and cryptocurrency objectives. Users can establish "Cash Goals" through the specialized "Cash Reserve" offering, designed for readily accessible funds. Additionally, "Crypto Goals" can be set up utilizing a dedicated Crypto ETF portfolio. It is important to note that these particular goal types operate under distinct frameworks and are therefore excluded from the scope of the investment allocation advice methodology discussed herein, which pertains to the strategic deployment of capital within broader investment portfolios.

For the vast majority of investment goals, with the notable exception of Emergency Funds, the combination of the anticipated time horizon and the selected goal type serves as critical inputs for Betterment’s algorithmic approach. This information informs the platform about when the user intends to access their funds and, importantly, their expected withdrawal strategy. For instance, a goal designated for a significant one-time purchase might necessitate a full and immediate liquidation of assets, whereas a retirement goal typically involves a series of periodic withdrawals over an extended period.

Emergency Funds, by their very nature, are designed to address unforeseen financial exigencies. Consequently, they do not possess a predetermined time horizon. While Betterment may assign a provisional time horizon for the purpose of providing initial saving and deposit guidance, this does not influence the recommended investment allocation. This flexibility is essential, as the timing and magnitude of an emergency expense are inherently unpredictable. Betterment acknowledges this by maintaining a modest operational cash allocation within automated investment portfolios across taxable accounts, Health Savings Accounts (HSAs), and Individual Retirement Accounts (IRAs). For comprehensive details regarding these specific allocations, users are encouraged to consult the official disclosures pertaining to their respective portfolios.

Strategic Allocation Based on Goal Type and Time Horizon

For all investment goals, excluding Emergency Funds, Betterment formulates a recommended investment allocation that is dynamically influenced by both the time horizon and the chosen goal type. This recommendation is the product of a sophisticated analytical process that involves projecting a spectrum of potential market outcomes. The optimal risk level is then determined by averaging the performance across the 5th to 50th percentiles of these projected market scenarios. This methodology aims to balance potential growth with a measured approach to risk.

In contrast, for Emergency Funds, Betterment’s recommended investment allocation is specifically engineered to foster growth potential while simultaneously mitigating the risk of significant drawdowns. The strategy aims to ensure that any potential decline in value does not erode the essential buffer needed to cover unexpected emergency expenses, maintaining a recommended buffer above the principal amount required.

Investment Allocation Ranges for Key Goal Types

Betterment provides clear ranges for recommended investment allocations across various goal types, excluding Emergency Funds. These ranges illustrate the strategic adjustments made based on the proximity to the goal’s completion and its inherent nature:

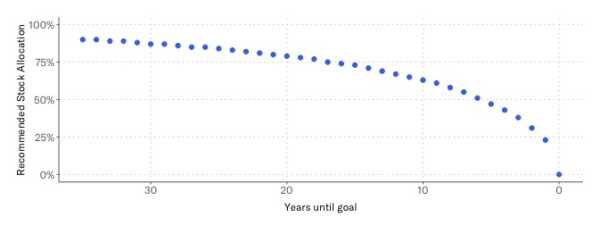

- Major Purchase: This category spans a broad spectrum of risk, from an aggressive 90% allocation to stocks for goals with a horizon of 33 years or more, down to a conservative 0% allocation to stocks when the time horizon has been reached, implying immediate liquidation.

- Education: Similar to Major Purchases, Education goals can be invested aggressively with up to 90% in stocks for long-term horizons (33+ years), gradually de-risking to 0% stocks as the educational milestone approaches.

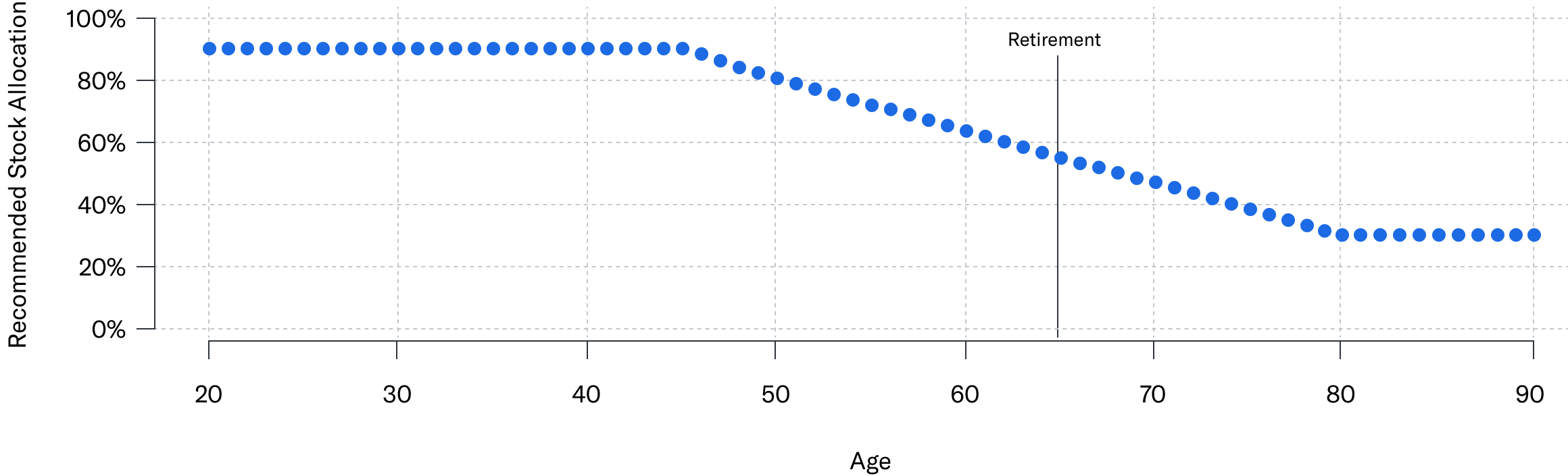

- Retirement: For retirement savings, the allocation begins at a robust 90% in stocks for those with 20 or more years until retirement age. As individuals approach their retirement age, the allocation becomes more conservative, reaching 56% stocks once retirement age is attained.

- Retirement Income: This category is designed for individuals already in or nearing retirement. It starts with a 56% stock allocation for those with 24 or more years of life expectancy remaining, progressively shifting towards a more conservative 30% stock allocation for individuals with nine years or less of remaining life expectancy.

- General Investing: For broader, less defined investment objectives, the allocation starts at a flexible 90% in stocks for horizons exceeding 20 years, and moderates to 56% stocks once the investment horizon is reached.

The "Glidepath": A Dynamic Allocation Strategy

The data presented in the table clearly illustrates a fundamental principle of investment strategy: the longer the time horizon for a goal, the more aggressive Betterment’s recommended allocation tends to be. Conversely, shorter time horizons necessitate a more conservative approach. This dynamic adjustment process over time is what Betterment refers to as a "glidepath." A glidepath is the predefined route an investment portfolio takes, gradually shifting its asset allocation from a more aggressive stance to a more conservative one as the investment goal approaches its target date.

Betterment offers visual representations of these glidepaths for different goal types, providing users with a clear understanding of how their investment allocation is expected to evolve.

Major Purchase and Education Goals Glidepath

The glidepath for Major Purchase and Education goals is characterized by a steady decrease in stock allocation as the target date draws nearer. This approach prioritizes capital preservation in the final stages, ensuring that funds are available for their intended use without being significantly impacted by market volatility. The accompanying graph visually depicts this downward trend, where the recommended stock allocation diminishes as the years until goal completion decrease.

Retirement and Retirement Income Goals Glidepath

The glidepath for Retirement and Retirement Income goals is more nuanced, reflecting the extended nature of retirement and the need for continued growth potential alongside income generation. For retirement, the allocation becomes more conservative as retirement age is reached, but it is designed to support withdrawals over a potentially long retirement span. The Retirement Income glidepath is particularly tailored for individuals who may be drawing income from their investments, often maintaining a higher allocation to growth-oriented assets for a longer duration compared to a simple liquidation goal. The provided illustration for retirement planning showcases a hypothetical scenario, emphasizing that actual client performance can vary due to market fluctuations and individual account adjustments.

General Investing Goals Glidepath

The glidepath for General Investing goals offers flexibility for long-term wealth accumulation. It allows for a more aggressive stance in the early years, leveraging the potential for higher returns from equities, and gradually shifts towards a more balanced portfolio as the investment horizon matures. This strategy aims to capture long-term market growth while progressively reducing risk as the capital is needed.

The "Auto-Adjust" Feature: Proactive Risk Management

To further support users in navigating these glidepaths, Betterment offers an "auto-adjust" feature. This functionality automates the process of modifying a goal’s allocation to manage risk as the investment timeline progresses. The system makes incremental adjustments, creating a smooth and predictable glidepath.

The "auto-adjust" feature is available for investment goals that have an associated time horizon, with the exception of Emergency Fund goals, the Target Income portfolio managed in conjunction with BlackRock, and the Goldman Sachs Tax-Smart Bonds portfolio. This feature is compatible with several of Betterment’s core portfolio offerings, including the Betterment Core portfolio, SRI portfolios, Innovation Technology portfolio, Value Tilt portfolio, and the Goldman Sachs Smart Beta portfolio. By enabling the "auto-adjust" feature during the acceptance of a recommended allocation, users opt for Betterment to automatically realign their investments with the predetermined glidepath. This is achieved through a combination of reactive rebalancing, which addresses deviations from the target allocation, and proactive rebalancing, which anticipates and manages upcoming shifts in the glidepath.

Adjusting for Individual Risk Tolerance

While Betterment’s recommended allocations and glidepaths are meticulously crafted based on "risk capacity"—the ability of a goal to withstand financial setbacks given its time horizon and withdrawal strategy—users retain the autonomy to deviate from these recommendations. Betterment acknowledges that individual comfort levels with risk can vary significantly.

To accommodate this, the platform incorporates an interactive slider tool. This intuitive interface allows clients to visually adjust their asset allocation, toggling between different proportions of stocks and bonds. Users can fine-tune their portfolio until they arrive at an allocation that aligns with their personal risk tolerance and their expectations for potential growth outcomes. Betterment categorizes risk tolerance into five distinct levels, enabling users to select a profile that best suits their psychological and financial comfort with market fluctuations. This personalized approach ensures that investment strategies are not only theoretically sound but also practically manageable and psychologically sustainable for each individual investor.

{kind=link}