When individuals engage with Betterment’s investment platform, a core feature empowers them to define and pursue specific financial objectives. This robust system allows for the creation of an unlimited number of investment goals, each meticulously tailored to the user’s aspirations. During the goal-setting process, users are prompted to specify the anticipated time horizon for each objective and to select a predefined goal type. This foundational step is critical, as it informs Betterment’s sophisticated allocation methodology, designed to align investment strategies with individual needs and timelines.

While the primary focus of this allocation advice revolves around traditional investment goals, Betterment also extends its offerings to encompass cash management through its Cash Reserve product and cryptocurrency investments via its Crypto ETF portfolio. These specialized accounts, though integral to a comprehensive financial strategy, operate under distinct allocation principles and are therefore outside the purview of the investment allocation methodology detailed herein.

For the vast majority of investment goals, with the notable exception of Emergency Funds, the user-defined time horizon and chosen goal type serve as crucial inputs. These parameters enable Betterment to understand not only when the funds are expected to be needed but also how they are anticipated to be withdrawn. For instance, a goal earmarked for a significant down payment on a property might necessitate a full, immediate liquidation of assets. Conversely, a retirement goal typically implies a strategy of partial, periodic liquidations over an extended period.

Emergency Funds represent a unique category. By their very nature, these funds lack a predetermined time horizon. While Betterment may assign a provisional time horizon during the initial setup to guide saving and deposit advice, this designation is mutable and critically, it does not influence the recommended investment allocation for the Emergency Fund itself. This approach acknowledges the inherent unpredictability of emergency expenses – their timing and magnitude are unknowable. To address this, Betterment maintains a modest operational cash allocation within its automated investing portfolios across taxable accounts, health savings accounts, and individual retirement accounts. Further details regarding these allocations are available within the specific disclosures pertaining to each portfolio.

The core of Betterment’s investment allocation strategy for all goals (excluding Emergency Funds) is predicated on a data-driven projection of market outcomes. The platform endeavors to identify the optimal risk level by averaging performance across the 5th to 50th percentiles of projected market scenarios. This methodology aims to strike a balance between potential growth and risk mitigation. For Emergency Funds, the recommended allocation prioritizes growth potential while simultaneously establishing safeguards against significant drawdowns, ensuring that the fund’s value remains above a recommended buffer relative to the immediate emergency need.

Recommended Investment Allocations by Goal Type

The following table outlines the spectrum of recommended investment allocations for various goal types, excluding Emergency Funds. These ranges are dynamic and adapt based on the interplay between the time horizon and the specific goal type selected by the user.

| Goal Type | Most Aggressive Recommended Allocation | Most Conservative Recommended Allocation |

|---|---|---|

| Major Purchase | 90% stocks (33+ years) | 0% stocks (time horizon reached) |

| Education | 90% stocks (33+ years) | 0% stocks (time horizon reached) |

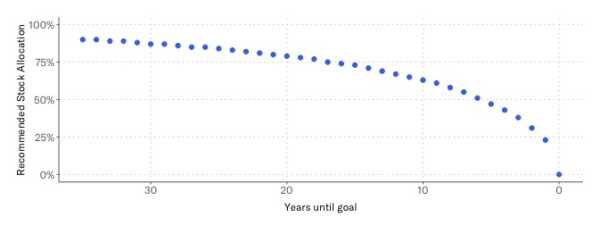

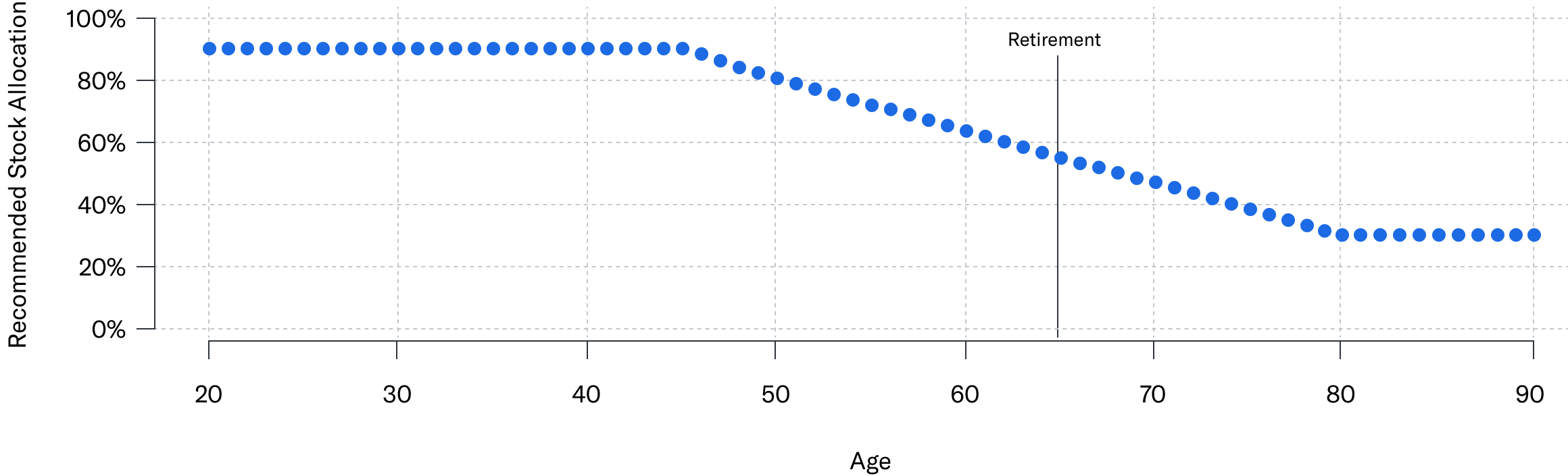

| Retirement | 90% stocks (20+ years until retirement age) | 56% stocks (retirement age reached) |

| Retirement Income | 56% stocks (24+ years remaining life expectancy) | 30% stocks (9 years or less remaining life expectancy) |

| General Investing | 90% stocks (20+ years) | 56% stocks (time horizon reached) |

This data clearly illustrates a fundamental principle in investment strategy: a longer time horizon generally correlates with a more aggressive recommended allocation, allowing for greater exposure to potentially higher-growth assets like stocks. Conversely, as a goal’s time horizon shortens, the recommended allocation becomes more conservative, emphasizing capital preservation and reducing exposure to market volatility. This gradual adjustment of the recommended allocation over time is commonly referred to as a "glidepath."

Understanding the Glidepath Mechanism

Betterment’s glidepath feature is designed to automatically adjust the recommended investment allocation for a given goal as it progresses toward its target date. This proactive risk management ensures that the portfolio’s composition evolves in tandem with the user’s proximity to accessing their funds.

For Major Purchase and Education Goals, the glidepath typically charts a course from a highly aggressive allocation (up to 90% stocks) for horizons exceeding 33 years, progressively decreasing stock allocation as the goal date approaches, reaching 0% stocks at the time horizon’s conclusion. This strategy is rooted in the expectation of a full liquidation of assets upon reaching the goal’s deadline.

For Retirement and Retirement Income Goals, the glidepath operates with a nuanced approach. For retirement savings, an allocation of up to 90% stocks is recommended for individuals with 20 or more years until retirement age. As retirement age is reached, this allocation gradually shifts to a more conservative stance, typically around 56% stocks. The Retirement Income glidepath, designed for individuals already in or nearing retirement, exhibits further refinement. It suggests an allocation of 56% stocks for those with 24 or more years of remaining life expectancy, tapering down to 30% stocks for those with 9 years or less. This extended timeframe for retirement income needs allows for a sustained, albeit managed, level of equity exposure to combat inflation and support long-term income generation.

The General Investing Goals glidepath mirrors aspects of retirement planning, starting with a potential 90% stock allocation for horizons exceeding 20 years and moderating to 56% stocks as the time horizon is reached. This category offers flexibility for long-term wealth accumulation without the specific withdrawal constraints of retirement.

The "Auto-Adjust" Feature: Dynamic Portfolio Management

To further facilitate the smooth progression along these glidepaths, Betterment offers an "auto-adjust" feature. This functionality automatically recalibrates a goal’s allocation to systematically manage risk as the investment timeline nears its end. The adjustments are made incrementally, creating a seamless and smooth glidepath experience.

The distinction between glidepaths for different goal types is significant. For instance, "Major Purchase" goals adopt a more conservative trajectory compared to "Retirement" or "General Investing" glidepaths. This is because the expectation for a major purchase is often a singular, immediate withdrawal of the entire invested sum. Therefore, minimizing risk as the date approaches is paramount. In contrast, retirement goals, which anticipate ongoing distributions, allow for a higher risk allocation even as the target retirement age is met, to support sustained income.

The auto-adjust feature is available for investment goals possessing an associated time horizon. It excludes Emergency Fund goals, as well as portfolios utilizing specific offerings like the Target Income built with BlackRock portfolio and the Goldman Sachs Tax-Smart Bonds portfolio. The auto-adjust functionality is compatible with the Betterment Core portfolio, SRI portfolios, Innovation Technology portfolio, Value Tilt portfolio, and the Goldman Sachs Smart Beta portfolio. Users have the option to enable this feature upon accepting Betterment’s recommended allocation. This feature employs both reactive and proactive rebalancing techniques to ensure the goal’s allocation remains aligned with the predetermined glidepath.

Adjusting for Individual Risk Tolerance

While Betterment provides robust, data-driven recommended allocations and glidepaths, the platform recognizes that individual risk tolerance is a deeply personal attribute. The aforementioned recommendations are primarily based on what Betterment terms "risk capacity." This concept quantifies a client’s ability to withstand financial setbacks, taking into account the goal’s time horizon and intended liquidation strategy. Clients are not bound by these recommendations and are encouraged to adjust their portfolios to align with their comfort levels.

To facilitate this personalization, Betterment incorporates an interactive slider. This tool allows users to dynamically adjust the allocation between different asset classes, such as stocks and bonds, until they arrive at an allocation that reflects their desired balance of potential growth and acceptable risk. Betterment categorizes risk tolerance into five distinct levels, providing a structured framework for users to navigate their choices. These categories are:

- Conservative: Prioritizes capital preservation with minimal exposure to market volatility.

- Moderately Conservative: A slight increase in risk tolerance compared to conservative, with a modest allocation to growth assets.

- Moderate: A balanced approach, seeking both growth and stability.

- Moderately Aggressive: Emphasizes growth potential with a higher allocation to riskier assets.

- Aggressive: Seeks maximum growth potential, accepting higher levels of market volatility.

By offering both sophisticated, automated glidepaths and intuitive tools for individual risk assessment, Betterment aims to provide a comprehensive and personalized investment experience, empowering users to confidently pursue their financial goals. This dual approach underscores the company’s commitment to democratizing sophisticated investment strategies and making them accessible to a broad range of investors. The platform’s continuous evolution in its allocation methodologies reflects a commitment to adapting to market dynamics and user needs, solidifying its position as a leader in the digital investment advisory space.

{kind=link}