Recent market sentiment has been dominated by a palpable concern: are stock prices, particularly within the technology sector, reaching unsustainable heights? A closer examination of key valuation metrics, such as the Shiller Price-to-Earnings (PE) ratio, reveals levels not seen since the speculative fervor of the dot-com era. Compounding these concerns are the substantial and increasingly intricate "circular" investments being made by major tech corporations, a strategy that carries inherent risks should the anticipated breakthroughs in Artificial Intelligence (AI) fail to materialize at the pace and scale currently projected. This confluence of elevated valuations and complex investment strategies has fueled widespread discussion about the possibility of an impending AI bubble, with some market commentators drawing parallels to the dramatic implosion of the dot-com market at the turn of the millennium. However, such comparisons do not automatically portend an inevitable crash or necessitate an immediate shift in investment strategies.

The nature of economic bubbles is such that their identification and prediction are inherently challenging. It is often only in hindsight that their existence can be definitively confirmed. Nevertheless, by examining historical precedents, investors can gain valuable context for the current market dynamics surrounding AI and refine their approaches to navigating potential volatility. This analysis will delve into the characteristics of market bubbles, explore key historical examples, and offer insights into how investors can position themselves to weather such cycles.

Defining the Bubble: When Enthusiasm Outpaces Reality

At its core, a financial bubble occurs when the price of an asset becomes significantly detached from its intrinsic value, driven by expectations of future growth that are exceedingly difficult, if not impossible, to achieve. While bubbles can manifest across various asset classes, they are frequently associated with periods of rapid technological innovation and widespread adoption. The challenge in identifying a bubble in real-time lies in the inherent uncertainty of future growth. What appears overvalued today could, in some cases, become justified by unforeseen advancements and market shifts. This ambiguity is precisely why definitive pronouncements about current bubbles are often only validated in retrospect.

Echoes of the Past: Lessons from the Dot-Com and Housing Bubbles

History offers potent case studies of speculative manias. The dot-com boom of the late 1990s and early 2000s serves as a prime example. This period was characterized by low interest rates, abundant capital, and the nascent stages of mass internet adoption. Companies could achieve astronomical valuations with little more than the inclusion of ".com" in their corporate name.

A quintessential illustration of this irrational exuberance was Pets.com. Despite being deeply unprofitable, spending a disproportionate amount on advertising, and losing money on every sale, the company launched its initial public offering (IPO) in February 2000. On its first day of trading, it commanded a market capitalization of $290 million, a figure it would never surpass. Within nine months, the company had ceased operations and began liquidating its assets. This phenomenon was not isolated; the Nasdaq Composite index, the favored exchange for many tech startups, surged by 178% from January 1998 to its peak in March 2000. Following this peak, the index experienced a precipitous decline, bottoming out at 1,114.11 in October 2002, a staggering 78% drop from its high.

It is crucial to reiterate that the certainty of a bubble’s existence often emerges only after its collapse. Some market observers point to a 1996 speech by then-Federal Reserve Chairman Alan Greenspan, where he coined the term "irrational exuberance," as an early indicator. While Greenspan’s warning proved prescient, market prices continued to ascend for several more years. Importantly, long-term investors who remained invested through the dot-com downturn still realized substantial returns. The US stock market, as measured by broad indices, delivered an annualized total return exceeding 8.5% in the decade following Greenspan’s speech, even accounting for the subsequent bear market. This underscores the principle that sustained market participation, even through periods of volatility, is key to long-term wealth accumulation.

More recently, the mid-2000s witnessed the dramatic implosion of the housing bubble. This period was also influenced by low interest rates, but critically, it was exacerbated by lax lending standards and complex financial engineering. Pools of subprime mortgages were bundled into securities that, despite their underlying risk, were often assigned favorable ratings by credit agencies. The prevailing sentiment was a deeply ingrained belief that home prices would never experience a broad decline. From July 2001 to July 2006, the Case-Shiller Home Price Index saw an increase of nearly 62%, equating to an annual growth rate of approximately 12%, significantly higher than the roughly 4% annual growth observed in preceding decades.

The inevitable reversal was severe. The index declined for over five years, eventually reaching a bottom in February 2012, more than 27% below its peak. As housing prices plummeted, borrowers with adjustable-rate mortgages, often featuring initial "teaser" rates, found themselves unable to refinance at affordable levels and struggled with their new, higher payments. This led to a surge in mortgage defaults and a catastrophic collapse in the value of mortgage-backed securities. Financial institutions with significant exposure to these markets, such as Bear Stearns and Lehman Brothers, faced existential crises. Bear Stearns was acquired by JPMorgan Chase in a distressed sale in early 2008, while Lehman Brothers declared bankruptcy in September 2008, a pivotal event that triggered a sharp decline in the S&P 500 index, which subsequently fell over 56% from its late 2007 highs before recovering its previous peak levels over approximately 5.5 years.

Common Threads and Enduring Lessons from Market Manis

Despite their distinct origins, both the dot-com and housing bubbles shared several critical characteristics:

- Systemic Impact: Both bubbles, while originating in specific sectors (technology and real estate/finance, respectively), ultimately exerted a significant negative influence on the broader US stock market.

- Sectoral Disparity: The fallout was not uniform. Sectors directly linked to the bubble’s genesis, such as technology and financial services, experienced the most severe declines.

- Eventual Recovery: In both instances, the US stock market demonstrated resilience and eventually recovered, albeit with varying recovery timelines.

- Long-Term Investor Rewards: Investors who maintained their positions throughout these turbulent periods continued to benefit from the historically robust long-term returns of equities.

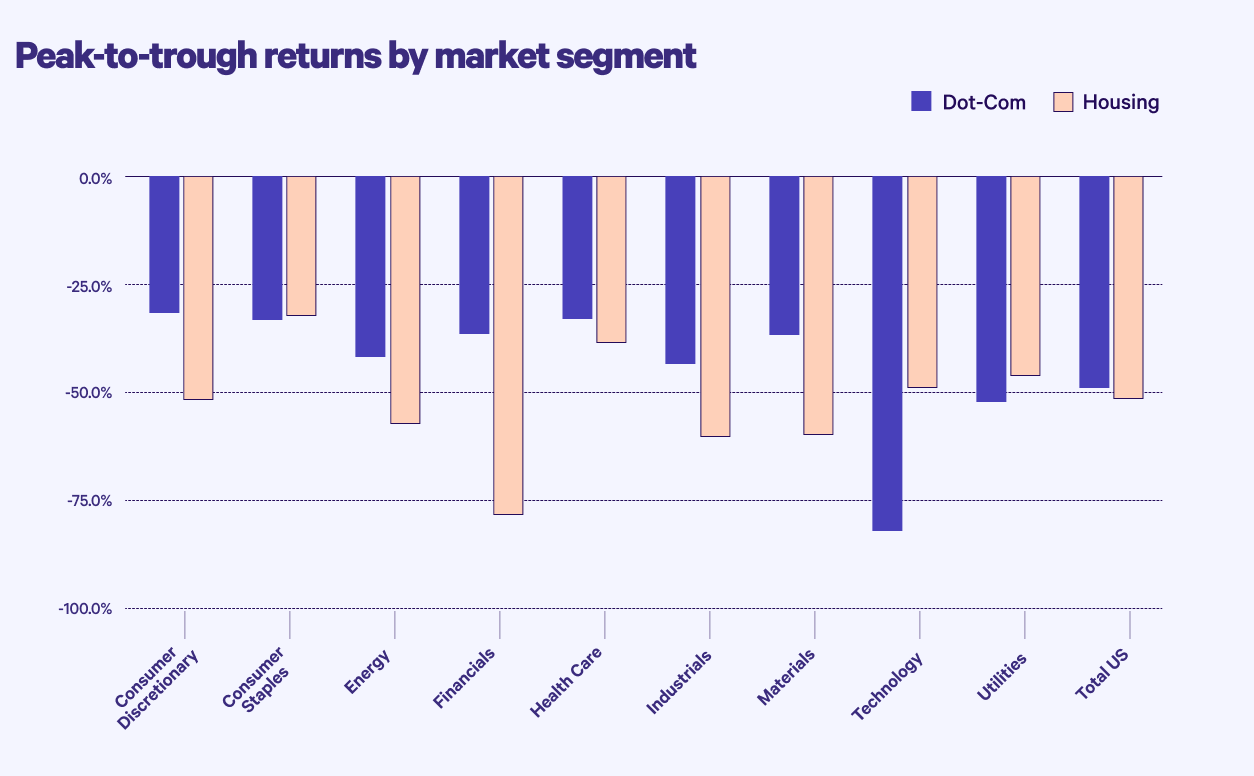

Illustrating the first two points, historical data shows that during the dot-com bust, the technology sector experienced a peak-to-trough decline of approximately 78%, while the broader US stock market saw a drawdown of around 49%. Following the housing crisis, the financial sector endured a similar magnitude of decline, with the overall market experiencing a drawdown of about 56%. These figures, drawn from sources like the Center for Research in Security Prices (CRSP), highlight the amplified losses within the epicenter of the bubble, but also the significant spillover effects onto the wider market. It is also noteworthy that less volatile asset classes, such as investment-grade corporate bonds, exhibited far more muted declines during these periods, underscoring the protective value of diversification.

The third and fourth points are vividly illustrated by analyzing the long-term performance of the US stock market. An investment of $1 in the US stock market in 1926, tracked by the Kenneth R. French Data Library, would have grown substantially by 2025. While the peaks and troughs of events like the dot-com and housing bubbles are discernible upon close inspection, they do not fundamentally alter the consistent upward trajectory of the market over extended periods. This sustained growth, often averaging between 7-10% annually over many decades, is a testament to the power of long-term investing and the capacity of the market to overcome even significant crises.

Navigating the Unpredictable: Strategies for a Volatile Landscape

Risk is an inherent and unavoidable component of investing. The pursuit of returns exceeding the risk-free rate necessitates taking on risk and enduring periods of market downturns and bear markets. The potential for bubbles to form and subsequently burst is simply one facet of this inherent investment risk.

While accurately predicting or completely avoiding bubbles is akin to market timing – an endeavor notoriously difficult to execute successfully – investors can implement strategies to mitigate their exposure. The cornerstone of such mitigation is diversification. For investors concerned about an overconcentration in AI-related assets, the most effective defense is to ensure their portfolios are broadly diversified across various asset classes, geographies, and sectors. This includes international investments, as significant allocations to AI are currently concentrated within the US market.

Consider the hypothetical investor heavily invested in Pets.com or Lehman Brothers; their outcomes would have been catastrophic. An investor with broader exposure to the technology sector or highly leveraged real estate might have fared better but still faced substantial losses. However, an investor holding a diversified broad market index fund would have experienced temporary pain but would have ultimately benefited from the market’s historical propensity to recover and generate generous long-term returns.

The temptation to forecast future market movements to gain an advantage is understandable. However, whether AI represents a true technological revolution or a speculative bubble remains unknowable and beyond individual investor control. Therefore, a more prudent approach focuses on the elements within an investor’s direct control: minimizing fees, optimizing tax efficiency, and managing risk through robust diversification. By diligently adhering to these principles, investors can build a resilient portfolio capable of navigating a wide spectrum of market conditions, including the potential formation and eventual bursting of speculative bubbles.