The pursuit of maximizing investment returns has long been a cornerstone of financial planning, with strategies like diversification, risk management, and tailored asset allocation playing pivotal roles. However, an often-overlooked yet potent method for enhancing after-tax returns lies in strategically utilizing investment losses. Betterment, a prominent digital investment advisor, has introduced a sophisticated, fully automated tool designed to leverage this strategy: Tax Loss Harvesting (TLH). This innovative approach aims to help investors get more out of their portfolios by turning temporary market dips into valuable tax advantages.

Tax loss harvesting, at its core, involves selling securities that have depreciated in value to realize a capital loss. This loss can then be used to offset capital gains, thereby reducing an investor’s tax liability. The challenge, however, lies in maintaining the desired asset allocation without triggering the IRS’s "wash sale" rule, which disallows a loss if a substantially identical security is repurchased within 30 days. Betterment’s TLH service addresses this complexity through a holistic approach, optimizing not only automated activities like rebalancing but also user-initiated transactions.

Understanding the Mechanics of Tax Loss Harvesting

Capital losses, when realized by selling a depreciated asset, offer a direct avenue to lower tax bills. These losses can first offset any capital gains incurred throughout the year. If losses remain after offsetting gains, up to $3,000 of ordinary income can be reduced annually. Any further losses can be carried forward indefinitely to offset future gains. While primarily a tax deferral strategy, its long-term benefits can significantly enhance overall portfolio performance.

The fundamental principle of tax loss harvesting is to sell a security at a loss and then immediately acquire a correlated, or similar, asset. This dual action achieves two critical objectives: it "harvests" a valuable tax loss and ensures the investor’s portfolio remains aligned with its target asset allocation. This strategy is not new to sophisticated investors, but Betterment’s implementation introduces innovations designed to overcome the limitations of traditional methods.

Navigating the Complexities of the Wash Sale Rule

The IRS’s wash sale rule is the primary hurdle in effective tax loss harvesting. This rule stipulates that if an investor sells a security and buys a "substantially identical" one within 30 days before or after the sale, the loss from the sale is disallowed. The rationale is to prevent investors from claiming a loss while maintaining continuous ownership of the underlying investment.

The wash sale rule’s reach is broad, extending beyond transactions within the same account. It also applies if a substantially identical security is purchased in an individual retirement account (IRA), a 401(k), or even a spouse’s account. This comprehensive application aims to prevent investors from circumventing the rule by using nominally different accounts. A particularly detrimental aspect is the treatment of wash sales involving IRAs or 401(k)s; while a disallowed loss in a taxable account is typically postponed, it can be permanently lost if the replacement security is purchased within a tax-advantaged account.

Historical Context of Tax Regulations: The wash sale rule has been a part of the U.S. tax code since the Revenue Act of 1921, underscoring the long-standing effort by tax authorities to prevent artificial loss generation. Its consistent application reflects a commitment to ensuring that tax deductions are based on genuine economic dispositions of assets.

Betterment’s Innovative Solution: Parallel Position Management

Traditional approaches to avoiding wash sales often involve either delaying reinvestment (leading to market exposure gaps), reallocating to entirely different asset classes (disrupting the desired allocation), or a "switchback" strategy where an investor repurchases the original security after 30 days. These methods have significant drawbacks. Delaying reinvestment means missing potential market gains, reallocating can skew portfolio balance, and switchbacks can inadvertently trigger short-term capital gains, potentially negating the tax benefits and even increasing tax liability.

Betterment’s solution hinges on its proprietary Parallel Position Management (PPM) system. This system maintains a suite of closely correlated securities within each asset class, comprising a primary, alternate, and sometimes a tertiary security. When a tax loss is harvested from the primary security, the proceeds are reinvested in the alternate security, which offers similar market exposure but is not considered "substantially identical" for wash sale purposes.

Key Features of Betterment’s PPM System:

- Parallel Securities: Betterment meticulously screens and selects primary and alternate securities based on factors like expense ratio, liquidity, tracking error, and crucially, covariance. This ensures that when one security is sold, its replacement closely mirrors its performance, minimizing tracking differences and maintaining portfolio integrity. The slight cost difference between primary and alternate securities is deemed negligible compared to the potential tax savings.

- PPM for All Transactions: The PPM system extends its tax-optimization capabilities beyond automated harvesting. It intelligently manages customer-initiated transactions, including withdrawals, deposits, and dividend reinvestments. When a customer withdraws funds, the system prioritizes selling assets that would incur the least tax liability, such as those with lower cost bases or that avoid short-term capital gains. For deposits, inflows are directed to underweight asset classes, and within those classes, to the primary security unless doing so incurs greater wash sale costs than purchasing the alternate.

- Wash Sale Management Across Accounts: A critical innovation is PPM’s ability to manage wash sale implications across both taxable and IRA/401(k) accounts. Recognizing that wash sales involving IRAs can permanently disallow losses, Betterment employs a tertiary ticker system. When a customer makes a deposit into their IRA, the system routes the funds to a tertiary security within the asset class, thereby avoiding any conflict with harvested losses in the taxable account. This ensures that realized losses are preserved, even when funds move between account types.

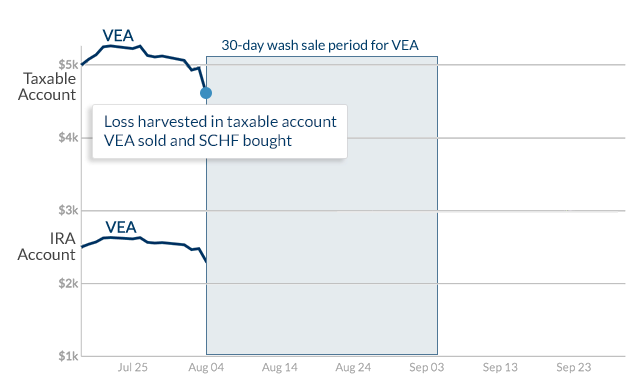

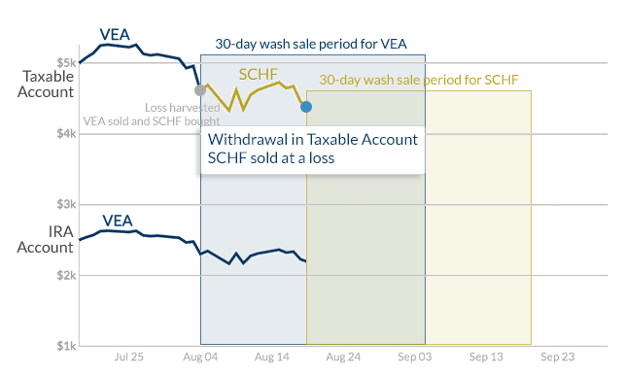

Example of Tertiary Ticker Usage:

Consider an investor with a Developed Markets ETF (VEA) in both their taxable and IRA accounts. Betterment harvests a loss in VEA within the taxable account and reinvests in a correlated ETF (SCHF). If the investor then withdraws funds from their taxable account and deposits them into their IRA, buying VEA or SCHF in the IRA would trigger a wash sale. Instead, Betterment’s system directs the IRA deposit into a tertiary ETF (IEFA) for Developed Markets, preserving the harvested loss in the taxable account and maintaining the desired allocation.

Model Calibration and Data-Driven Decisions

Betterment’s tax loss harvesting algorithm is not a static rule-based system; it is continuously calibrated and optimized using rigorous Monte Carlo simulations. This forward-looking approach tests the model’s performance across tens of thousands of potential market scenarios, aiming to optimize effectiveness based on expected future returns and volatility.

The decision to harvest a loss is based on a threshold where the potential benefit, net of costs, exceeds a predefined level. Costs considered include trading expenses (embedded in Betterment’s wrap fee), execution expenses (e.g., bid-ask spreads), and any increased cost of ownership for the replacement asset. By factoring in these elements, the system aims for a net positive outcome from each harvesting event.

Who Benefits Most from Tax Loss Harvesting?

Tax loss harvesting is primarily a tax deferral strategy, meaning that while it can reduce current tax liabilities, it generally results in higher capital gains when the assets are eventually sold. The true value is realized through tax deferral, allowing reinvested savings to compound over time.

Beneficiary Profiles:

- High-Income Earners: Individuals in higher tax brackets can realize substantial immediate savings by offsetting capital gains or by deducting up to $3,000 of capital losses against ordinary income. For those in high-tax states, this deduction can translate into significant annual tax reductions.

- Investors with Consistent Capital Gains: Those who regularly generate capital gains from selling appreciated assets, whether from other investments or real estate, can directly utilize harvested losses to offset these gains, leading to immediate and substantial tax savings.

- Long-Term Investors: The longer the deferral period, the greater the benefit of tax loss harvesting, as the tax savings have more time to grow through compounding.

- Philanthropists: Investors who plan to donate appreciated securities to charity or pass them on to heirs can avoid capital gains taxes altogether. When combined with tax loss harvesting, this strategy offers a powerful way to maximize wealth transfer and charitable giving.

Who May Benefit Less:

- Those Expecting Lower Future Tax Brackets: If an investor anticipates being in a significantly lower tax bracket in the future, tax deferral may be less advantageous than realizing gains now at a lower rate.

- Investors with Scattered Portfolios: If an investor holds the same or similar assets outside of Betterment, it can be challenging to manage wash sale rules effectively across all accounts, potentially negating the benefits of TLH within Betterment.

- Rapid Liquidators: Investors planning to liquidate their entire portfolio in a short timeframe might see the aggregated capital gains push them into a higher tax bracket, diminishing the overall benefit.

Quantifying the Value: Betterment’s Estimated Tax Savings Tool

To provide clients with tangible insights into the impact of tax loss harvesting, Betterment offers an "Estimated Tax Savings" tool within their online accounts. This tool leverages transactional data from Betterment accounts and client-provided demographic and financial information to generate dynamic estimates of both current-year and cumulative tax savings.

The tool meticulously analyzes tax-lot level trading data, categorizing harvested losses and offsetting them against capital gains and ordinary income according to IRS rules. It factors in individual tax situations, including income levels, state of residence, filing status, and the IRS cap on ordinary income offsets.

Methodology:

- Client-Centric Modeling: Estimates are personalized using self-reported income, state, filing status, and dependents to determine federal and state income tax rates, capital gains rates, and standard deductions.

- IRS Offset Hierarchy: The tool adheres to the IRS’s prescribed order for offsetting gains and losses, ensuring accurate calculations.

- Current Year vs. All-Time Savings: The tool distinguishes between estimated savings for the current tax year (based on realized offsets) and all-time savings (projecting potential savings from all harvested losses, assuming they will be offset by gains at current tax rates).

It is crucial to note that these figures are estimates and not guarantees. Actual tax outcomes depend on individual tax returns, market performance, and other factors not captured by the tool. Betterment advises consulting with a personal tax advisor to determine the suitability of tax loss harvesting for one’s specific circumstances.

Conclusion

Betterment’s fully automated tax loss harvesting strategy represents a significant advancement in making sophisticated tax-efficiency tools accessible to a broader range of investors. By meticulously managing the complexities of wash sale rules and leveraging parallel securities, the platform aims to enhance after-tax returns without introducing additional downside risk. While the strategy is primarily about tax deferral, its long-term benefits, particularly for higher earners and long-term investors, can be substantial, empowering individuals to navigate the tax landscape more effectively and optimize their investment outcomes.

{kind=link}