Financial services are growing more complex, which means that risk, compliance, and governance are no longer simply back-office functions. These services, which were once considered “boring” aspects of fintech, are now core to how banks and fintechs operate, compete, and scale. From evolving regulatory expectations to increasingly sophisticated fraud and operational risks, financial institutions are under constant pressure to maintain control while continuing to innovate. The shift is profound: GRC (Governance, Risk, and Compliance) has transformed from a cost center into a strategic enabler, vital for maintaining trust, ensuring stability, and driving sustainable growth in a rapidly digitalizing world.

The Evolving Landscape of Financial GRC

For decades, governance, risk management, and compliance were largely manual, siloed processes within financial institutions. Compliance departments often operated reactively, scrambling to interpret new regulations and implement changes, while risk teams grappled with increasingly complex models and data sets. The advent of digital banking, the proliferation of fintechs, and the global interconnectedness of financial markets have exponentially amplified these challenges.

The volume and velocity of regulatory changes are staggering. Industry reports indicate that the average financial institution tracks thousands of regulatory updates annually across multiple jurisdictions. Non-compliance is not merely a theoretical threat; it carries severe penalties, including hefty fines, reputational damage, and even operational restrictions. For instance, global financial institutions have paid billions in fines related to AML (Anti-Money Laundering) and KYC (Know Your Customer) violations alone in recent years. Beyond financial penalties, the erosion of public trust can have long-lasting, detrimental effects on customer acquisition and retention.

Moreover, the nature of risk itself has broadened. Cyber threats, data breaches, and sophisticated fraud schemes pose an existential danger. Operational risks, stemming from complex IT systems, third-party vendor dependencies, and human error, are equally pressing. The adoption of advanced technologies like Artificial Intelligence (AI) and Machine Learning (ML) introduces new layers of complexity, requiring robust governance frameworks to ensure fairness, transparency, and accountability, particularly as regulators worldwide begin to establish specific guidelines for AI ethics and risk management in financial services, such as the EU’s AI Act or proposed frameworks in the US.

Against this backdrop, the traditional, manual approach to GRC is simply unsustainable. It is costly, inefficient, prone to error, and unable to keep pace with the dynamic environment. Financial institutions are thus compelled to seek out innovative, technology-driven solutions that can automate processes, provide real-time insights, and integrate GRC functions across the entire organization.

FinovateSpring 2026: A Nexus for Innovation in GRC

FinovateSpring 2026, a premier event in the financial technology calendar, serves as a critical platform for showcasing the latest advancements shaping the future of finance. Held annually, Finovate events are renowned for their unique demo-focused format, where innovative companies present their solutions live, without slides or pre-recorded videos, directly to an audience of financial institution executives, investors, and media. This direct, transparent approach allows for immediate assessment of technology’s practical applications and potential impact.

For the 2026 iteration, the spotlight on Governance, Risk, and Compliance solutions underscores the strategic importance these areas have gained. The event provides a crucial forum for banks and fintechs to discover technologies that can help them navigate the intricate web of regulatory requirements, mitigate emerging risks, and build resilient, future-proof operations. The companies presenting at FinovateSpring 2026 are not just offering tools; they are offering strategic partnerships to transform how financial institutions approach these core functions, moving them from reactive compliance to proactive risk intelligence and strategic governance. This shift is critical for banks looking to not only survive but thrive in an increasingly regulated and competitive market.

Spotlight on GRC Innovators at FinovateSpring 2026

A new group of companies at FinovateSpring 2026 is demonstrating how banks can modernize governance, streamline compliance, and better manage risk across the organization. These innovators are helping financial institutions move toward a more proactive, automated, and scalable approach to GRC.

CRIF

CRIF, a global leader in credit bureau services, analytics, and decisioning platforms, is at the forefront of modernizing credit risk management. With over three decades of experience, CRIF offers a broad suite of services that empower financial institutions to make smarter, faster, and more transparent lending decisions. In an era where speed to market and precision in credit assessment are paramount, CRIF’s technology enables banks and lenders to design, test, and deploy sophisticated credit strategies with unprecedented speed and control. The platform uniquely combines diverse data sources, advanced analytics, and robust governance mechanisms into a single, cohesive framework.

A key differentiator for CRIF is its commitment to accessibility and explainability. The platform features no-code strategy design, allowing business users, not just data scientists, to configure and adapt credit policies, significantly reducing reliance on IT departments and accelerating deployment cycles. Real-time simulations with key performance indicator (KPI) validation ensure that new strategies are rigorously tested before going live, minimizing unforeseen risks. Furthermore, CRIF integrates embedded AI agents that support compliant and explainable decisioning. This is particularly vital as regulatory bodies increasingly demand transparency and auditability in AI-driven processes, ensuring that lending decisions are fair, unbiased, and justifiable. Headquartered in Italy and founded in 1988, CRIF serves a global clientele of banks, credit unions, fintechs, and lenders, providing them with the tools to navigate complex credit landscapes while maintaining stringent regulatory confidence. Their approach allows for agility without compromising on the necessary rigor required in credit risk management.

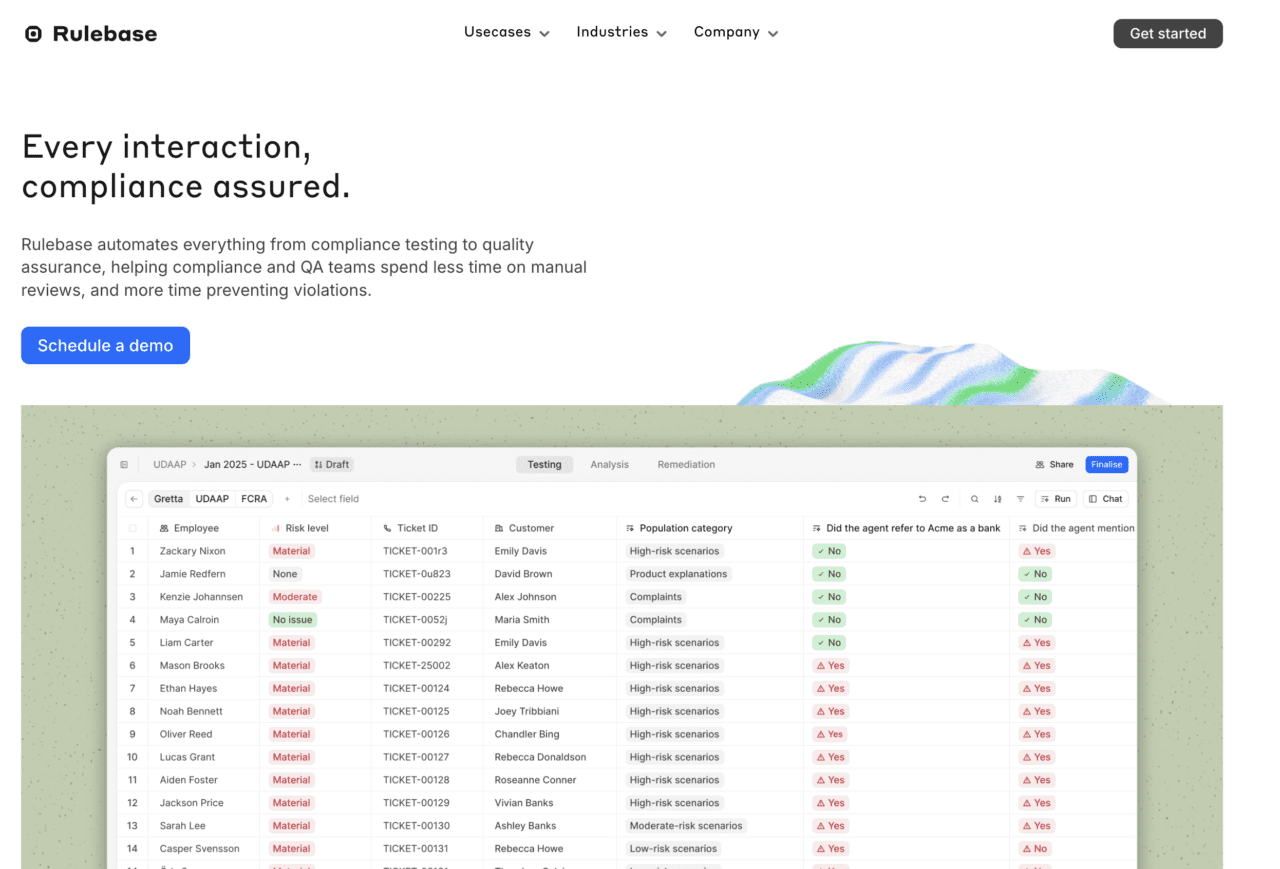

Rulebase

Rulebase addresses a critical pain point for financial institutions: scaling compliance in an environment of constant change and increasing customer interactions. The New York-based company, founded in 2025, offers a modern platform that automates testing and quality assurance across customer touchpoints and internal workflows. Traditionally, compliance testing has been a manual, labor-intensive, and often retrospective process, prone to human error and limited in scope. Rulebase fundamentally transforms this by introducing continuous monitoring capabilities.

Its platform actively observes activity, leveraging advanced analytics to detect potential violations in real-time or near real-time. This proactive detection mechanism allows institutions to address issues before they escalate into significant compliance breaches. Beyond mere detection, Rulebase automatically generates audit-ready evidence, meticulously documenting compliance activities and providing an indisputable record for regulatory scrutiny. This capability is invaluable, as it frees compliance teams from the arduous task of compiling evidence manually, enabling them to shift their focus from reactive data gathering to proactive risk mitigation and strategic oversight. By significantly improving the speed and accuracy of compliance operations while simultaneously reducing regulatory risk, Rulebase empowers organizations to allocate their human capital to higher-value activities, ensuring that compliance is not merely a burden but an integrated, efficient component of day-to-day operations.

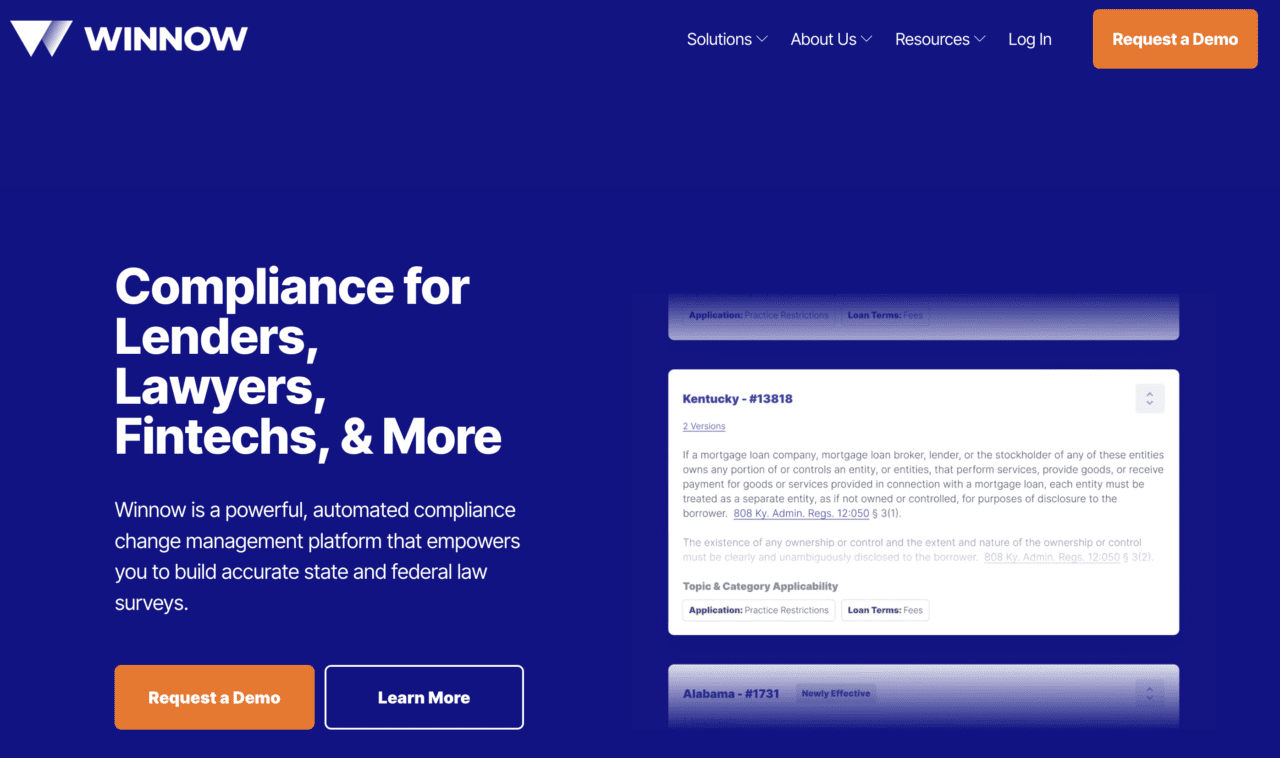

Winnow

Winnow, headquartered in Anaheim, California, and founded in 2018, tackles the pervasive challenge of regulatory complexity head-on. Financial institutions often struggle with fragmented regulatory information, relying on manual research, legal counsel, and disparate internal systems to interpret and meet their compliance obligations. This traditional approach is not only time-consuming and expensive but also susceptible to inconsistencies and misinterpretations. Winnow’s solution centralizes and streamlines compliance by providing a single, easy-to-use platform that replaces these inefficient methods.

The core of Winnow’s offering is its delivery of tailored, attorney-reviewed regulatory guidance. This means financial institutions receive precise, actionable insights relevant to their specific operations and jurisdictions, eliminating the need to sift through mountains of generic legal texts. By leveraging expert legal analysis and intuitive technology, Winnow enables organizations to quickly understand their compliance duties, significantly reducing the time and cost associated with traditional legal and compliance research. The platform’s ability to reduce complexity and improve accuracy allows compliance teams to dedicate less time to interpreting dense regulations and more time to actively implementing and executing against them. In a world where regulatory changes are constant and often nuanced, Winnow provides a more efficient and reliable path to maintaining compliance, offering a strategic advantage in a highly regulated environment.

The Electronic Guardian

The Electronic Guardian, a Pittsburgh-based company founded in 2019, introduces an innovative value proposition for financial institutions by addressing the growing need for secure digital asset management and estate planning. Its flagship platform, The Coop, serves as a secure digital repository designed to help individuals organize, protect, and transfer critical financial and personal information. In an increasingly digital world, individuals accumulate a vast array of digital assets and important documents, from cryptocurrency keys and online account credentials to wills, insurance policies, and property deeds. Managing these assets, particularly in the context of legacy planning, has become a complex challenge.

The Coop consolidates these disparate documents and assets into a centralized, highly secure system. This not only aids in personal organization but also evolves into a comprehensive estate inventory, seamlessly supporting legacy planning and ensuring asset continuity for beneficiaries. Security is paramount, and The Electronic Guardian employs private encryption and "at rest" recoverability features, guaranteeing that sensitive information remains both secure from unauthorized access and reliably accessible to designated parties when it matters most – for instance, during an emergency or after the passing of an account holder. By offering tools like The Coop, banks, credit unions, and insurance providers can deliver significant added value to their clients. This not only creates a potential new revenue stream but also strengthens client relationships by associating the financial institution with safety, security, and foresight in personal and estate management, fostering deeper trust and loyalty.

Model IQ by Kevin D. Oden & Associates

As financial institutions increasingly rely on sophisticated analytical models for everything from credit scoring and fraud detection to capital planning and risk assessment, the governance of these models has become a critical regulatory and operational concern. Model IQ, developed by Kevin D. Oden & Associates, addresses this challenge directly with an automated platform designed to manage model risk and ensure compliance with stringent regulatory requirements. Founded in 2018 and headquartered in San Francisco, Model IQ is built by "quants" (quantitative analysts) for the industry, ensuring a deep understanding of the technical and regulatory nuances involved.

The solution is specifically tailored to streamline compliance with key guidelines such as SR 11-7 (Supervisory Guidance on Model Risk Management), FDIC, and NCUA requirements. These regulations mandate rigorous validation, documentation, and ongoing monitoring of all models used by financial institutions. Model IQ brings much-needed structure, speed, and consistency to what can otherwise be a cumbersome and manual model risk management (MRM) process. The platform automates the entire model lifecycle, from development and validation to deployment and ongoing performance monitoring. This automation accelerates review timelines, drastically improving efficiency, while simultaneously enhancing accuracy and audit readiness. By providing a scalable approach to governance in an increasingly model-driven industry, Model IQ serves a diverse client base, from community credit unions to regional banks and fintechs, enabling them to confidently leverage advanced analytics while meeting their regulatory obligations and mitigating the inherent risks associated with complex models.

The Strategic Imperative for Modern GRC

The demonstrations at FinovateSpring 2026 underscore a fundamental truth: risk, compliance, and governance are no longer merely cost centers but central to a bank’s operations, directly impacting an organization’s ability to scale, innovate, and compete. The past decade has seen global financial institutions incur hundreds of billions of dollars in fines for compliance failures, alongside significant reputational damage. The cost of managing compliance has also surged, with some estimates placing global spending on regulatory technology (RegTech) in the tens of billions of dollars annually, and this figure is projected to grow substantially.

As banks adopt advanced technologies like AI and machine learning, expand their digital channels, and operate across increasingly complex regulatory environments, the volume and velocity of risk have increased to a point where manual processes and siloed systems can no longer keep up. The reliance on human intervention for tasks that can be automated not only introduces inefficiencies but also heightens the risk of errors and oversight. This creates an operational burden on internal teams, diverting valuable resources from strategic initiatives to repetitive, labor-intensive GRC activities.

Platforms that automate compliance testing, improve decision transparency, and streamline model risk management offer banks a powerful way to stay ahead of regulators while operating more efficiently. By embracing these technological advancements, financial institutions can move from a reactive, defensive posture to a proactive, strategic one. This transformation allows them to anticipate regulatory changes, identify potential risks before they materialize, and integrate ethical considerations into their technological advancements. Moreover, the ability to demonstrate robust, automated GRC frameworks can become a significant competitive advantage, enhancing investor confidence and attracting clients who value security and reliability.

For end-users, the benefits extend beyond the institutional level. Solutions like The Electronic Guardian highlight how GRC principles can translate into tangible value for consumers. Having a secure, organized place to store and manage key financial and personal documents is crucial for both security and organization, particularly in an era of growing digital footprints and increasing cybersecurity threats. Financial institutions that offer such tools as a benefit will not only add a potential revenue stream but will also give clients another compelling reason to associate them with safety, security, and comprehensive financial well-being. This demonstrates how advanced GRC solutions can foster deeper customer relationships and enhance the overall value proposition of financial service providers.

Broader Implications for the Financial Ecosystem

The innovations showcased at FinovateSpring 2026 signal a broader shift in the financial ecosystem. The rise of RegTech is not just about compliance; it’s about making financial institutions more agile, resilient, and trustworthy. These technologies facilitate better data management, predictive analytics for risk, and automated reporting, which can also pave the way for more efficient supervisory technology (SupTech) used by regulators themselves. This convergence promises a future where compliance is embedded by design, rather than bolted on as an afterthought.

Furthermore, the collaboration between established financial institutions and nimble fintechs specializing in GRC solutions is becoming critical. Banks gain access to cutting-edge technology and expertise, while fintechs benefit from the scale and market access of traditional players. This symbiotic relationship accelerates the pace of innovation, ensuring that the financial industry remains robust and capable of serving a diverse and evolving global clientele. The long-term implications include reduced operational costs across the industry, a stronger defense against financial crime, enhanced consumer protection, and ultimately, a more stable and trusted global financial system. The emphasis on GRC at events like FinovateSpring 2026 confirms that these functions are no longer just about adherence to rules, but about building the foundation for innovation and sustainable success in the digital age.