In the realm of wealth management, the concept of "asset location" is frequently lauded as a nearly cost-free strategy to enhance investment performance. At its core, asset location leverages the distinct tax treatments of different account types—taxable, tax-deferred, and tax-exempt—to optimize the after-tax returns of an investment portfolio without altering its overall risk profile. This sophisticated approach involves strategically placing less tax-efficient assets in accounts that offer greater tax advantages and more tax-efficient assets in those with less favorable tax structures, all while maintaining the desired aggregate asset allocation.

The Nuances of Investment Taxation and the Quest for Higher Returns

Maximizing the after-tax return on investments is a complex undertaking for many individuals. While contributing to tax-advantaged accounts like IRAs and 401(k)s (available in traditional or Roth versions) is a well-understood method for reducing immediate tax burdens, the subsequent decision of what to invest within these accounts often receives less meticulous consideration. Millions of Americans accumulate savings across a combination of these qualified accounts and taxable brokerage accounts, typically funding the latter only after exhausting contribution limits for the former. However, the tax implications of investment choices within each account type are critical for enhancing the overall after-tax value of one’s savings.

The fundamental principle of asset location hinges on the differential tax efficiency of various investment vehicles and the varying degrees of tax shelter offered by different account types. By intelligently aligning these factors, investors can potentially increase their net returns. This strategy is applicable to nearly all investors who hold assets in more than one account type.

Asset Allocation: The Foundation, Asset Location: The Optimization

It is crucial to distinguish asset location from asset allocation. Asset allocation, the initial step, involves determining the optimal mix of asset classes—such as stocks and bonds—to align with an investor’s financial goals, risk tolerance, and time horizon. For instance, retirement planning typically dictates a portfolio tilted towards growth assets for younger investors and a more conservative allocation for those nearing retirement.

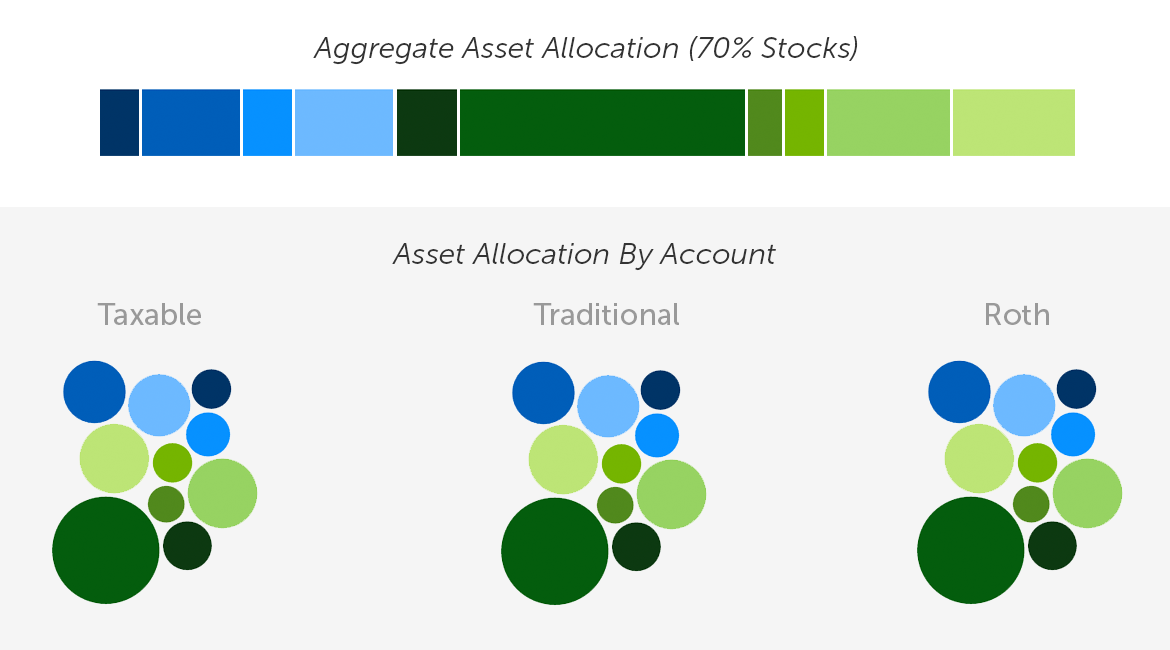

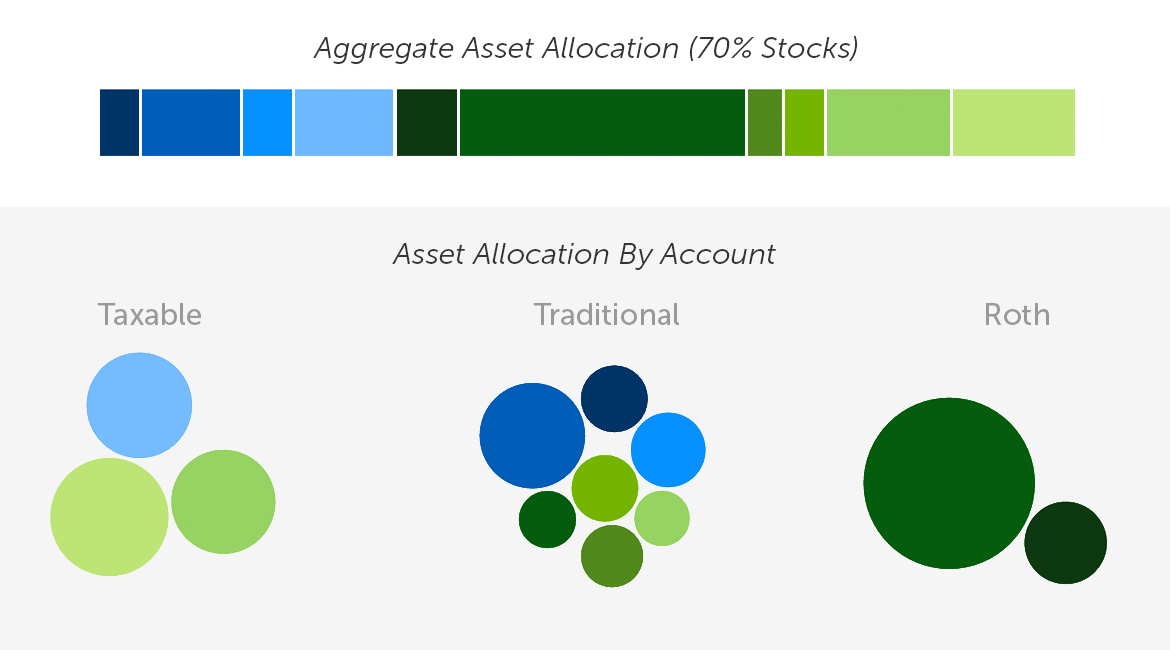

A common, though not always optimal, practice is to replicate the target asset allocation within each individual investment account. While this ensures the aggregate portfolio aligns with the investor’s goals, it overlooks the potential for tax optimization. Asset location, applied after the asset allocation has been established, seeks to enhance the after-tax performance of the overall portfolio by strategically distributing assets across available accounts based on their tax characteristics.

Understanding Tax Efficiency and Its Impact on Investment Returns

A key concept in asset location is "tax efficiency," which refers to an investment’s ability to generate returns with minimal "tax drag." Tax drag represents the annual erosion of investment returns due to taxes, particularly from income distributions like dividends. Investments that generate significant taxable income annually are considered less tax-efficient.

Taxable Accounts: In a taxable brokerage account, investment returns are subject to taxation either annually on distributions (dividends) or upon sale (capital gains). There are generally two main categories of investment income: dividends and capital gains. Dividends are typically taxed annually, contributing to tax drag. Capital gains, on the other hand, are taxed only when the asset is sold. Long-term capital gains (assets held for over a year) are generally taxed at preferential rates, while short-term capital gains (assets held for a year or less) are taxed at ordinary income rates. This distinction highlights the advantage of tax deferral for capital gains, allowing the invested capital to compound over longer periods.

Tax-Deferred Accounts (TDAs): Accounts like traditional IRAs and 401(k)s offer tax deferral. While investment growth within these accounts is not taxed annually, all distributions upon withdrawal in retirement are taxed at ordinary income rates. This means that while annual tax drag is eliminated, the eventual tax liability can be substantial, especially if the investor is in a higher tax bracket during retirement. The benefit of tax deferral is most pronounced for assets that generate significant annual taxable income, such as bond dividends.

Tax-Exempt Accounts (TEAs): Accounts such as Roth IRAs and Roth 401(k)s provide the most significant tax advantage. Investments grow tax-free, and qualified withdrawals in retirement are also tax-free. This makes TEAs exceptionally valuable for maximizing after-tax returns. The primary challenge with TEAs is managing their limited capacity and deciding which assets offer the greatest benefit when all taxes are eliminated.

Debunking Common Asset Location Myths

Several misconceptions surround asset location, leading some investors to overlook its potential benefits or implement it incorrectly.

-

Myth 1: Asset location is a one-time event. In reality, asset location is a dynamic process. Changes in market conditions, expected returns, dividend yields, tax laws, and crucially, the relative balances of the investor’s accounts (due to contributions, rollovers, or conversions) necessitate ongoing adjustments to maintain optimal location.

-

Myth 2: Asset location dictates account funding decisions. Asset location optimizes the placement of assets within existing accounts. It should not influence decisions about which accounts to fund. The choice between a traditional and Roth account, for instance, is primarily driven by an individual’s outlook on their future tax bracket compared to their current one.

-

Myth 3: Asset location is ineffective for small accounts. While the impact may be less pronounced, even a small account can offer significant optimization opportunities. For example, a substantial taxable balance combined with a small tax-exempt account could allow for the placement of high-growth, tax-inefficient assets in the tax-exempt account, yielding disproportionate benefits.

-

Myth 4: No value if only qualified accounts exist. Even with only traditional and Roth IRAs, asset location offers benefits. Tax-exempt accounts are superior to tax-deferred ones. Placing assets with the highest expected growth in the tax-exempt account, and managing required minimum distributions from the tax-deferred account, can enhance after-tax returns and provide greater control over future taxable income.

-

Myth 5: Bonds always belong in IRAs. This is an oversimplification. While bonds are often tax-inefficient due to their interest income, their optimal location depends on a nuanced analysis of their expected return, the specific tax treatment of interest income, and the investor’s overall account structure.

Advanced Asset Location Methodologies and Their Implications

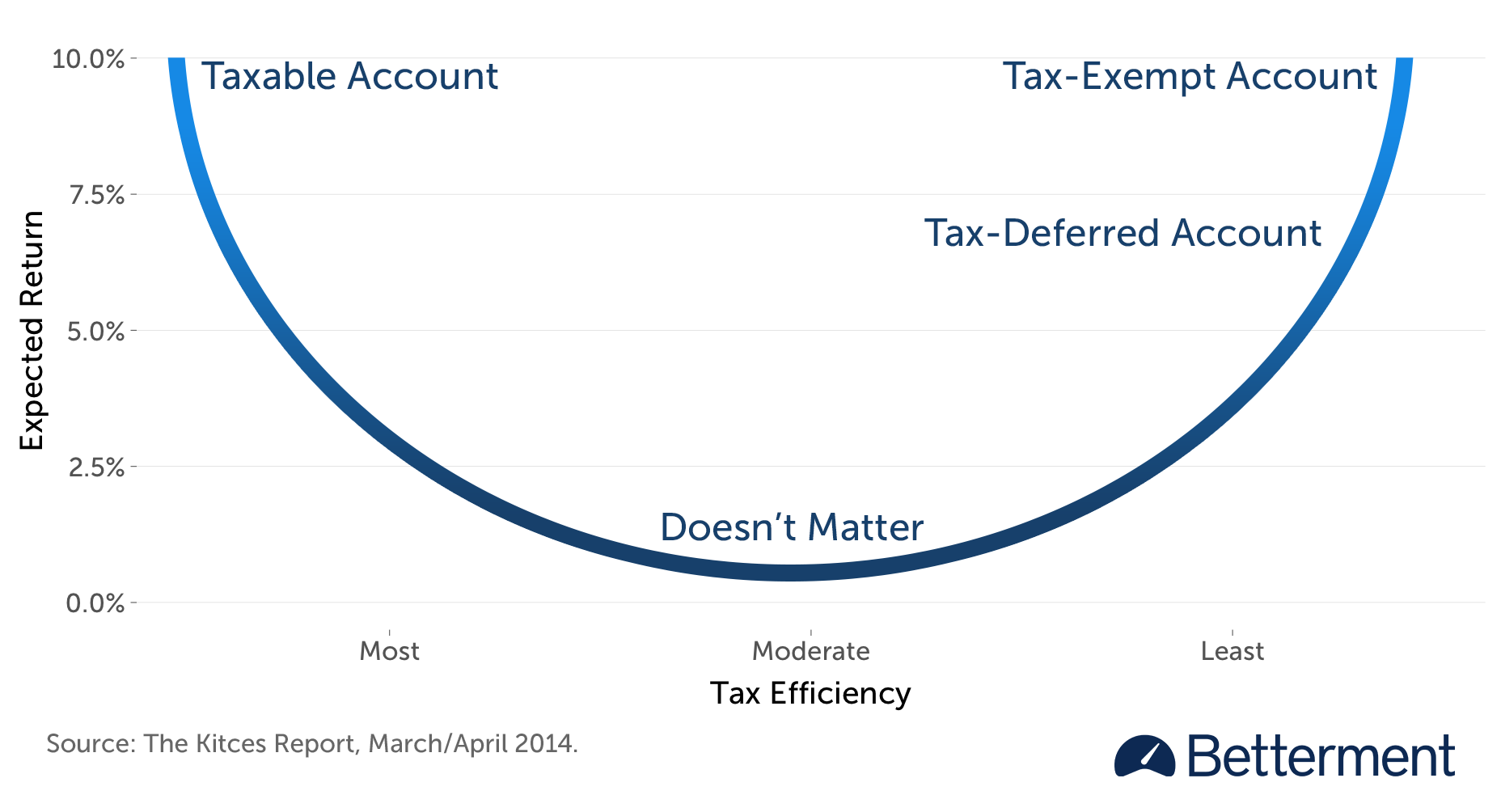

Sophisticated asset location strategies move beyond simplistic rules to incorporate a multi-faceted analysis of tax efficiency, expected returns, and the impact of liquidation taxes. Researchers like Michael Kitces have developed frameworks that visualize these relationships, often depicted as a "smile" curve. Assets with high expected returns and high tax efficiency are best placed in taxable accounts. Conversely, high expected return, highly tax-inefficient assets are candidates for tax-advantaged accounts, prioritized by the tax-exempt account first.

The Tax-Coordinated Portfolio (TCP) Methodology: Financial technology firms like Betterment employ advanced algorithms to implement asset location through features like their Tax-Coordinated Portfolio (TCP). This methodology utilizes linear optimization to maximize the after-tax value of an investor’s aggregate portfolio. The process involves:

- Deriving Account-Specific After-Tax Returns: For each asset class, an expected after-tax return is calculated for every account type, considering factors like dividend yields, tax rates, and the time horizon.

- Defining the Objective Function: This function mathematically represents the total after-tax value of the portfolio, incorporating the after-tax returns of each asset in each account and the amounts invested.

- Establishing Constraints: These constraints ensure that the total allocation to each asset class and the total investment within each account do not exceed the available resources.

- Linear Optimization: The algorithm solves for the optimal allocation of each asset across all available accounts, maximizing the objective function while adhering to the defined constraints.

This computational approach allows for precise asset placement, dynamically adjusting as account balances and market conditions evolve. It also integrates with other tax-management strategies like tax-loss harvesting, aiming for a holistic approach to tax efficiency.

Testing and Results: The Quantifiable Benefits of Asset Location

To validate the efficacy of advanced asset location strategies like TCP, rigorous testing is essential. Methodologies often involve Monte Carlo simulations, which model thousands of potential market scenarios to project the long-term after-tax performance of the strategy compared to a benchmark of uncoordinated portfolios.

Key Findings from Simulation Studies:

-

Higher Bond Allocations Yield Greater Alpha: Portfolios with a larger allocation to bonds tend to experience a more significant increase in after-tax returns when asset location is employed. This is because bonds are generally less tax-efficient than stocks, making them prime candidates for tax-advantaged accounts. However, this is not an endorsement for reducing stock allocations, as stocks are expected to generate higher absolute returns over the long term.

-

Presence of Roth Accounts Enhances Benefits: The availability of both taxable accounts and tax-exempt accounts (Roth IRAs) creates the most substantial opportunities for optimization. The contrast between these two ends of the tax spectrum allows for greater "account arbitrage."

-

Impact on Existing Accounts: For investors enabling asset location on existing taxable accounts with built-in capital gains, the immediate benefit may be less pronounced due to the need to avoid realizing those gains. However, ongoing contributions and dividend reinvestments will gradually shift the portfolio towards its optimal location.

Special Considerations and Nuances

While asset location offers substantial advantages, certain investor profiles and situations require careful consideration:

-

Low Tax Bracket Taxpayers: Individuals in the lowest tax brackets may not benefit significantly from asset location, as the tax arbitrage opportunities are diminished. In such cases, the focus might shift from tax efficiency to maximizing growth.

-

Accounts with Differing Time Horizons: Asset location is most effective when applied to accounts with similar intended withdrawal timelines, such as those designated for retirement. Applying it to accounts with materially different time horizons or those earmarked for emergency withdrawals can lead to suboptimal outcomes.

-

Large Upcoming Transfers or Withdrawals: Significant cash flows into or out of accounts can necessitate rebalancing, potentially triggering taxes. It is often advisable to delay enabling tax coordination until after these transactions have occurred, unless the deposits are into a taxable account, in which case immediate coordination is recommended.

-

Behavioral Challenges: Strategically placing assets with different volatility profiles across accounts can lead to differentiated movements in account balances. Investors must be prepared for this, understanding that while the aggregate portfolio’s risk remains consistent, individual account performance may diverge.

-

Interaction with Tax-Loss Harvesting (TLH): Asset location and TLH can work in tandem. Advanced systems ensure that TLH opportunities are preserved while assets are strategically relocated. The precise interaction depends on individual circumstances, with asset allocation forming the top tier, followed by asset location, and then TLH within the taxable account.

The Future of Asset Location: HSA Integration and Ongoing Evolution

As of May 2020, Health Savings Accounts (HSAs) can be integrated into Tax-Coordinated Portfolios. HSAs function similarly to Roth accounts, offering tax-free growth and tax-free withdrawals for medical expenses, making them highly advantageous for long-term savings. The inclusion of HSAs further expands the opportunities for tax optimization.

The field of asset location is continuously evolving, driven by advancements in financial technology and a deeper understanding of tax law. While no strategy guarantees specific outcomes, sophisticated asset location, when properly implemented, offers a powerful mechanism for investors to enhance their long-term, after-tax investment returns.

This article is for informational purposes only and does not constitute tax advice. Investors should consult with their personal tax advisor to determine the suitability of any investment strategy for their individual circumstances.