CaixaBank, one of Spain’s largest financial institutions, has officially secured authorization from the Comisión Nacional del Mercado de Valores (CNMV), Spain’s securities regulator, to operate as a Crypto Asset Service Provider (CASP) under the European Union’s groundbreaking Markets in Crypto-Assets (MiCA) Regulation. This pivotal approval marks a significant milestone not only for CaixaBank but also for the Spanish financial landscape, as it positions the bank alongside its two primary competitors, BBVA and Santander, in offering regulated digital asset services. With this authorization, CaixaBank has completed the trifecta of Spain’s "big three" banks now licensed to engage with the burgeoning crypto economy, signaling a decisive shift towards the integration of digital assets within conventional banking frameworks across the continent.

The granted license empowers CaixaBank to provide a comprehensive suite of crypto asset services, including the crucial functions of crypto custody, facilitating the transmission and execution of client orders, and enabling secure client transfers of digital assets. The bank has indicated its strategic intent to progressively roll out these services to its extensive customer base over the forthcoming months, meticulously planning the integration into its existing digital banking ecosystem. This move is a natural progression for CaixaBank, which has already been dipping its toes into the digital asset space by offering Bitcoin Exchange Traded Product (ETP) investments through its digital banking platform and its youth-focused imagin application. Furthermore, CaixaBank is a prominent member of the Qivalis consortium, a collaborative initiative involving twelve leading European banks dedicated to the development and eventual issuance of a euro-linked stablecoin, underscoring its long-term commitment to digital currency innovation.

The Race Among Spain’s Banking Giants: A Chronology of Crypto Adoption

CaixaBank’s entry into the regulated crypto market follows a discernible trend set by its Spanish peers, illustrating a broader strategic alignment within the country’s financial sector to embrace digital assets. The journey began with BBVA, which emerged as an early adopter among European financial institutions. In July 2025, BBVA officially launched its crypto services in Spain, building upon its earlier pilot programs and its established presence in Switzerland’s crypto banking sector. BBVA’s initial offerings focused on Bitcoin and Ethereum trading and custody for private banking clients, emphasizing a secure and regulated environment for high-net-worth individuals to access digital assets. This move was largely seen as a strategic response to evolving client demands and a proactive step to explore new revenue streams in a rapidly digitizing financial world.

Following BBVA’s pioneering efforts, Santander, another Spanish banking titan, made its significant foray into the crypto market through its digital-first subsidiary, Openbank. While Santander’s primary banking operations initially remained more cautious, Openbank’s agile structure allowed for a quicker deployment of innovative services. In September 2025, Openbank launched cryptocurrency trading services in Germany, strategically choosing a market with a relatively high appetite for digital assets and a clear regulatory outlook. Weeks later, leveraging the experience and infrastructure developed in Germany, Openbank expanded its crypto offerings to Spain, making a range of cryptocurrencies available for trading and custody to its Spanish clientele. Openbank’s approach underscored the growing importance of digital-native platforms within established banking groups to pilot and scale new services.

CaixaBank’s recent authorization therefore completes this strategic alignment among Spain’s three largest banks. While perhaps later to the full CASP licensing, CaixaBank’s existing engagements, such as offering Bitcoin ETPs and its involvement with the Qivalis stablecoin initiative, demonstrate a methodical and considered approach to market entry. Their planned rollout in the coming months is expected to integrate these new services seamlessly into their extensive retail and institutional offerings, leveraging their significant market share and established client relationships. This synchronized movement by Spain’s banking elite highlights a collective recognition of the irreversible shift towards digital finance and the imperative to remain competitive by offering a full spectrum of financial services, including those pertaining to crypto assets.

Understanding the MiCA Regulation: A Landmark Framework for Europe

The European Union’s Markets in Crypto-Assets (MiCA) Regulation stands as a monumental legislative achievement, representing the world’s first comprehensive regulatory framework specifically designed for crypto assets. Its genesis lies in the urgent need to address the fragmented and often uncertain regulatory landscape that characterized the European crypto market prior to its implementation. Before MiCA, individual EU member states adopted disparate approaches to regulating crypto, leading to regulatory arbitrage, market inefficiency, and inconsistent consumer protection. The primary objectives of MiCA are multifaceted: to foster innovation within the crypto space, ensure financial stability, protect consumers and investors, and maintain market integrity across the EU’s single market.

MiCA’s scope is broad, covering a wide array of crypto assets that are not already classified under existing financial legislation, such as securities or e-money. It meticulously categorizes crypto assets into different types, including asset-referenced tokens (ARTs), e-money tokens (EMTs), and other crypto assets, each with specific regulatory requirements. A cornerstone of MiCA is its stringent regulation of Crypto Asset Service Providers (CASPs), which include entities offering services like custody, exchange, advice, and portfolio management related to crypto assets.

Key pillars of MiCA for CASPs include:

- Authorization Requirements: CASPs must obtain authorization from a national competent authority in an EU member state, which then allows them to "passport" their services across the entire EU.

- Operational Resilience: Requirements for robust IT systems, security protocols, and business continuity plans to ensure reliable service delivery.

- Governance and Internal Controls: Mandates for sound governance arrangements, including clear organizational structures, effective risk management procedures, and measures to prevent conflicts of interest.

- Client Asset Segregation: Strict rules requiring CASPs to segregate client funds and crypto assets from their own proprietary assets, safeguarding client holdings in case of insolvency.

- Market Abuse Rules: Provisions against insider trading, market manipulation, and other illicit activities, mirroring those in traditional financial markets.

- Information Disclosure: Requirements for white papers, marketing communications, and ongoing disclosures to ensure transparency and informed decision-making for investors.

The implementation timeline for MiCA has been phased. Rules concerning stablecoins (ARTs and EMTs) came into effect earlier, around mid-2024, given their potential implications for financial stability. The full CASP regime, including the authorization process for service providers, became effective later in 2024 or early 2025, allowing for a transition period. The fact that Spanish banks are now receiving these licenses in 2026 confirms the full operationalization of the CASP framework.

A particularly noteworthy aspect of MiCA, and one that significantly benefits traditional financial institutions like CaixaBank, BBVA, and Santander, is the streamlined path for existing credit institutions. Under MiCA, banks that are already authorized and supervised under conventional financial regulations (like the EU’s Capital Requirements Directive or the Payment Services Directive) are not required to undergo a full, protracted CASP application process. Instead, they need only notify their respective national competent authority (such as Spain’s CNMV) a mere 40 days before commencing their crypto asset services. This expedited process is a pragmatic design choice, recognizing that banks already possess robust regulatory frameworks, capital requirements, anti-money laundering (AML) and counter-terrorist financing (CTF) protocols, and governance structures that largely align with MiCA’s objectives. This provision significantly lowers the barrier to entry for established financial players, encouraging them to bring their institutional rigor and client protection standards to the nascent crypto market.

The Broader European Landscape: Banks Embracing Crypto Under MiCA

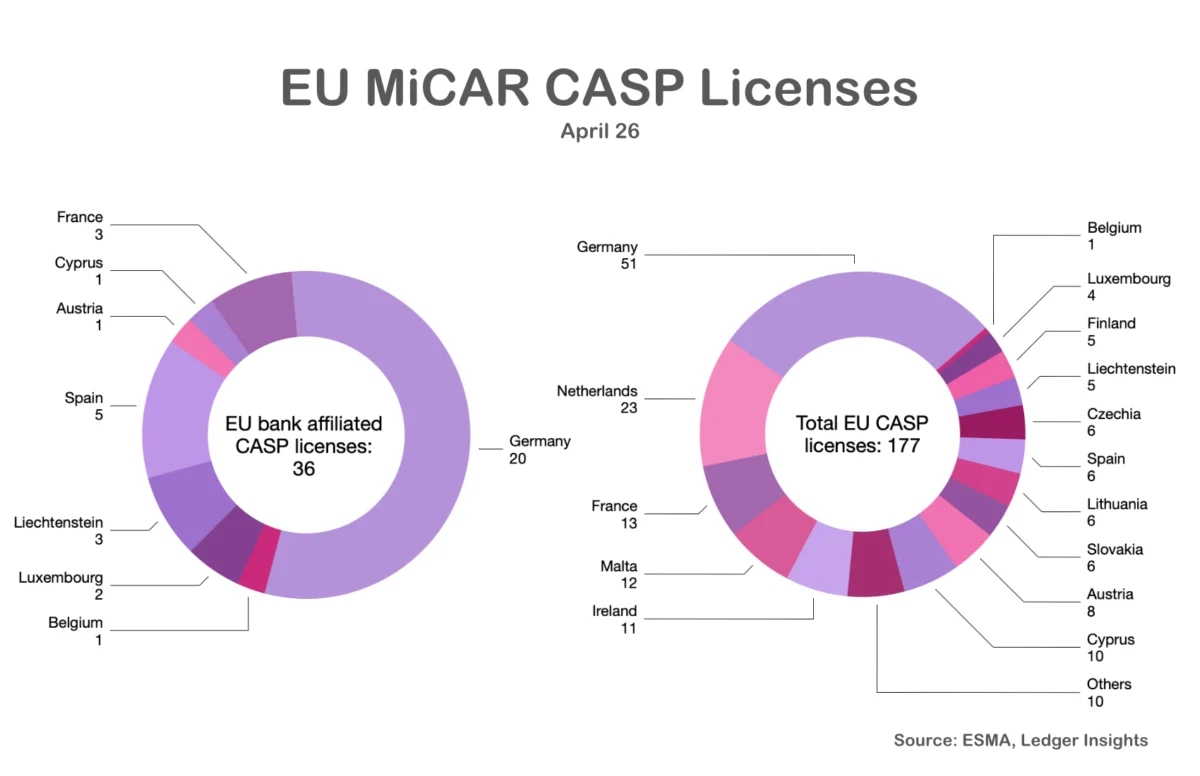

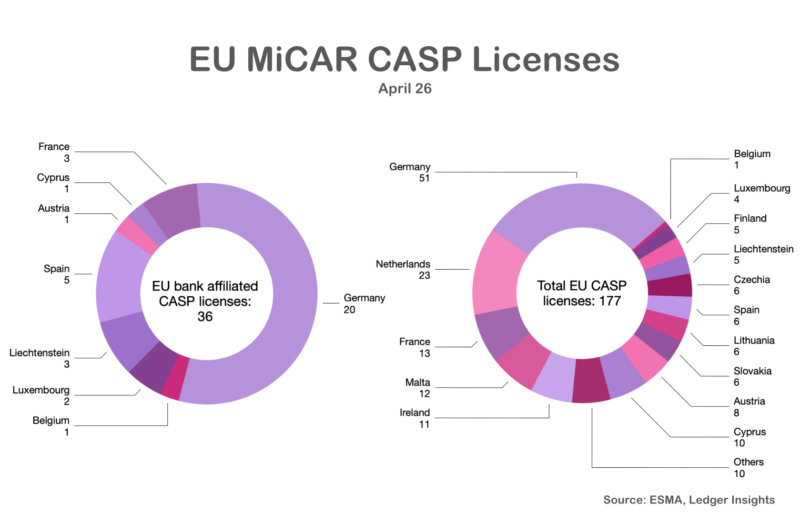

CaixaBank’s authorization is not an isolated event but rather a reflection of a wider trend across the European Union. Of the 177 CASP licenses awarded across the EU to date, a substantial 36 have gone to banks. This proportion, while still representing a minority of total licenses, is nevertheless significant and points to the strategic importance traditional financial institutions are placing on digital assets. The streamlined MiCA path is undoubtedly a major contributing factor to this uptake, but the motivations for banks extend deeper.

Traditional financial institutions are increasingly driven by several factors to embrace crypto:

- Client Demand: A growing segment of retail and institutional clients are expressing interest in holding, trading, and utilizing crypto assets. Banks are responding to this demand to retain and attract customers.

- Competitive Pressure: The rise of crypto-native exchanges and fintechs offering digital asset services has put pressure on incumbent banks to innovate and diversify their offerings to avoid losing market share.

- Revenue Diversification: Crypto services present new potential revenue streams through trading fees, custody fees, and the development of new tokenized products.

- Technological Innovation: Engagement with blockchain and distributed ledger technology (DLT) allows banks to explore efficiencies in payments, settlements, and asset management, potentially revolutionizing core banking processes.

- Risk Management under Regulation: MiCA provides a clear regulatory framework, which significantly reduces the compliance and reputational risks previously associated with engaging in the unregulated crypto market. Banks, by their nature, are risk-averse, and a defined regulatory perimeter is crucial for their participation.

While the opportunities are substantial, banks also face unique challenges. Integrating complex blockchain infrastructure with legacy IT systems can be technically demanding and costly. Furthermore, ensuring full compliance with MiCA, alongside existing financial regulations (e.g., AMLD6, GDPR), requires significant investment in specialized personnel, technology, and compliance frameworks. Despite these hurdles, the long-term strategic advantages, particularly in a regulated environment, appear to outweigh the complexities for a growing number of European banks.

Services Offered by Licensed Banks: Beyond Basic Trading

The scope of services that licensed banks like CaixaBank are authorized to provide under MiCA is comprehensive, extending far beyond simple cryptocurrency trading.

- Custody Services: This is perhaps one of the most critical offerings for institutional and high-net-worth clients. Secure custody involves the safekeeping of clients’ crypto assets, protecting them from theft, loss, or unauthorized access. Banks are expected to provide institutional-grade solutions, often leveraging a combination of cold storage (offline, hardware-based wallets) and hot storage (online wallets for active trading) with robust multi-signature security protocols and comprehensive insurance coverage. The segregation of client assets from the bank’s own funds is a strict MiCA requirement, offering an unparalleled level of protection compared to many unregulated crypto exchanges.

- Order Transmission and Execution: Banks facilitate the buying and selling of crypto assets on behalf of their clients. This involves receiving client orders, transmitting them to various liquidity venues (exchanges, over-the-counter desks), and executing them in a manner that ensures "best execution" – obtaining the most favorable terms available for the client. This service leverages the banks’ existing trading infrastructure and expertise in managing complex financial markets.

- Client Transfers: This service encompasses the seamless movement of crypto assets between clients, or between clients and other authorized service providers. Crucially, it also includes the critical "on-ramp" and "off-ramp" functionalities, allowing clients to convert fiat currency (e.g., Euros) into cryptocurrencies and vice versa. This integration is vital for bridging the gap between traditional finance and the digital asset economy, making crypto more accessible and liquid for mainstream users.

Beyond these core services, banks are also exploring and developing other digital asset-related offerings. CaixaBank’s involvement in the Qivalis consortium for a euro-linked stablecoin exemplifies this. Such stablecoins, backed by fiat currency and issued by regulated entities, promise to revolutionize payments and settlements by offering the stability of fiat with the efficiency of blockchain technology. Furthermore, the future could see banks playing a significant role in the tokenization of traditional assets (real estate, equities, bonds), creating new liquidity pools and investment opportunities, all within MiCA’s regulatory embrace.

Implications for the Market and Consumers: Mainstreaming Digital Assets

The increasing involvement of major banks like CaixaBank, BBVA, and Santander in the regulated crypto space carries profound implications for the broader financial market and for consumers across Europe.

- Mainstreaming Crypto: The most immediate impact is the significant step towards mainstreaming crypto assets. When established, trusted financial institutions begin offering crypto services, it lends considerable legitimacy to the asset class. This can attract a new wave of institutional investors and cautious retail clients who were previously hesitant due to regulatory uncertainty or perceived risks associated with less regulated platforms.

- Enhanced Consumer Protection: MiCA, enforced by national regulators and supported by the robust frameworks of banks, dramatically enhances consumer protection. Clients of licensed banks benefit from stringent operational, security, and governance standards, clear disclosure requirements, and avenues for redress. This stands in stark contrast to the often-risky environment of unregulated crypto platforms, where fraud, hacks, and mismanagement have historically been prevalent.

- Increased Competition and Innovation: The entry of traditional banks into the crypto market intensifies competition, potentially leading to better services, lower fees, and more innovative product offerings across the entire digital asset ecosystem. While crypto-native firms might face new competitive pressures, the increased market size and legitimacy could also create new partnership opportunities.

- Financial Stability: By bringing crypto assets under a comprehensive regulatory umbrella, MiCA, through the participation of regulated entities, contributes to greater financial stability. It reduces systemic risks associated with opaque, unregulated markets and ensures that major players adhere to capital requirements and risk management protocols.

- Spain’s Emergence as a Hub: With all three of its major banks now licensed, Spain is rapidly solidifying its position as a significant hub for regulated crypto services within the EU. This could attract further investment, talent, and innovation to the country’s financial technology sector.

Regulatory Oversight and Future Outlook

The role of national competent authorities, such as Spain’s CNMV, is critical in enforcing MiCA and ensuring that licensed CASPs, including banks, adhere to the highest standards. Beyond national oversight, the European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) play crucial roles in harmonizing MiCA’s implementation across member states, issuing guidelines, and ensuring consistent interpretation of the regulation. This multi-layered regulatory architecture aims to create a truly unified and secure digital asset market across the EU.

For CaixaBank, the "roll out in coming months" will likely involve a phased approach, potentially starting with specific client segments (e.g., private banking, institutional clients) before expanding to its broader retail base. This cautious yet strategic deployment will allow the bank to fine-tune its offerings, scale its infrastructure, and gather client feedback.

Looking ahead, the long-term vision is one of a fully integrated digital asset ecosystem within the EU, where traditional finance and blockchain technology converge. MiCA, coupled with the active participation of major banks, is paving the way for a future where digital assets are not just an alternative investment but an intrinsic part of the financial system, offering new efficiencies, greater accessibility, and enhanced opportunities for economic growth. The entry of CaixaBank, completing the roster of Spain’s banking heavyweights, is a powerful testament to this transformative journey.

Conclusion

CaixaBank’s successful acquisition of a MiCA CASP license from the CNMV is a landmark development, completing the triumvirate of Spain’s largest banks now offering regulated crypto asset services. This strategic move, following BBVA and Santander’s earlier entries, underscores a collective commitment from traditional financial institutions to integrate digital assets into mainstream finance. The comprehensive MiCA framework, with its streamlined path for banks, has been instrumental in facilitating this transition, promising enhanced consumer protection, increased market legitimacy, and greater financial stability across the European Union. As CaixaBank prepares to roll out its services, the Spanish financial sector, under the robust umbrella of MiCA, is poised to play a pivotal role in shaping the future of regulated digital asset services, marking a new era of convergence between traditional banking and the innovative world of cryptocurrencies.

{kind=link}